Since 2016, taxpayers paying a fee to the Platon system in relation to “heavy trucks” with a carrying capacity of more than 12 tons have the right to reduce the transport tax for each vehicle by the amount of the payment for this vehicle for the tax period (paragraph 12, paragraph 1, Art. 362 of the Tax Code).

The excess of the specified fee over the transport tax is recognized as an expense and reduces the income tax for the tax (reporting) period (subparagraph 49 of paragraph 1 of article 264, paragraph 48.21 of article 270 of the Tax Code of the Russian Federation). The same procedure is provided for with respect to the single tax under the simplified tax system (clause 37 of clause 1 of article 346.16 of the Tax Code of the Russian Federation).

The procedure for 1C to reflect the board on the system “PLATO”

So, we will consider the procedure in the program 1C 8.3 Accounting for the reflection of fees on the system "Plato" and its automatic application as a deduction to reduce the transport tax.

Step 1. Register a vehicle

Information on the fact that the car is registered in the Plato system has been added to the vehicle registration card. Based on this information, a tax entry will automatically appear on the application of the deduction on the cost of the fee to the Platon system:

Step 2. Transfer of the advance payment to the payment account in the Platon system

Step 3. Registration of the report from the operator of the Platon system for the month in 1C 8.3

The document is located in the Purchases section - the Journal Reports of the Platon system operator. It can be filled automatically by the Fill button:

As a result of the transaction, the following transactions are formed:

- Offset credit;

- On reflection of the cost of damage for federal roads on the basis of paragraph 5.18 of PBU 10/99 (in accounting);

- On the formation of expenses on account 97.21 “Prepaid expenses” (in tax accounting) until the tax (advance payment) is calculated.

At the end of the tax (reporting) period, the positive difference between the fee to the Platon system and the amount of the transport tax (advance payment on it) can be taken into account in income tax expenses on the basis of clause 49 of article 264 of the Tax Code of the Russian Federation:

Also, a record of the fee is entered in the accumulation register Expenses for "Plato".

Step 4. Routine operation. Transport tax calculation.

It is formed at the end of each tax (reporting) period. The document calculates the transport tax (advance payments), taking into account the amount of tax deduction, based on the fee paid according to the Platon system:

Traffic on the regulatory document Calculation of transport tax in 1C 8.3:

Help-calculation of transport taxin 1C 8.3 is the result of the regulatory operation "Calculation of transport tax" and can be used as a tax register for transport tax.

The form is available in the section Operations - Closing of the month and can be generated from the routine operation Calculation of transport tax or from the list of references - calculations:

Step 5. Fill out the transport tax declaration

The calculated tax with the deduction taken into account is reflected in the transport tax declaration in the new form approved by Order of the Federal Tax Service of Russia dated 05.12.2016 No. MMV-7-21 / 668:

Reflection of fees in expenses taken into account when calculating income tax (OSNO)

If the fee to the Platon system turns out to be more than the calculated tax, then the excess amount can be taken into account in the expenses when calculating income tax (paragraph 49, paragraph 1, article 264, paragraph 48.21, article 270 of the Tax Code) or a single tax for USN, (paragraph 37 of clause 1 of article 346.16 of the Tax Code).

In the program 1C 8.3 Accounting, the reflection of the amount of excess road tolls in tax expenses is reflected in the same Regulatory operation “Transport Tax Calculation”. Movement for this document:

For those who apply PBU 18/02, the amount by which the calculated transport tax was reduced for each individual vehicle with a carrying capacity of more than 12 tons is reflected in the costs as a constant difference:

Reflection of fees in the costs taken into account when calculating the single tax (STS)

Registration of tolls on federal roads in organizations on the USN is made by the same document, “Report of the operator of the Platon system. The document generates the postings:

- by offsetting the advance payment;

- to reflect in accounting as part of the costs of the damage caused to federal roads (paragraph 5.18 PBU 10/99):

- to reflect in the expenses for the simplified tax system, the entries in the accumulation register "Expenses for" Plato "will be used:

The routine operation “Calculation of transport tax” for the tax (reporting period) calculates the transport tax and, in the case of excess of the cost of harm to federal roads over the transport tax, reflects the amount of excess in KUDiR:

If, as a result of the calculation, the transport tax turns out to be higher than the fare on federal roads, then the amount of the transport tax will be charged in accounting:

And it will also be reflected in the tax register "Costs under the simplified tax system":

A taxpayer may reduce the amount of transport tax calculated at the end of the tax period for each vehicle by the amount of the Platon fee calculated in the current period in relation to this vehicle. About how to reflect in "1C: Accounting 8" a decrease in the transport tax on fees to the Platon system BUKH.1C was told by 1C experts.

When you purchase a vehicle and register it with the traffic police, the organization becomes a payer of transport tax (Article 357, Clause 1, Article 358 of the Tax Code of the Russian Federation).

Transport tax rates are determined by regional legislation, you can find them in the tax office at the place of registration of the vehicle. In this case, the base rates for transport tax are defined in Art. 361 of the Tax Code of the Russian Federation.

According to paragraph 1 of Art. 359 of the Tax Code of the Russian Federation the definition of the tax base depends on the type of vehicle.

When purchasing a truck, the organization pays tax based on the formula: Tax base * Tax rate * Decreasing coefficient, determined in accordance with paragraph 3 of Art. 362 of the Tax Code of the Russian Federation.

In addition, this formula also includes another indicator that reduces the amount of accrued transport tax - the payment for compensation for damage caused to roads, it is established by Part 5 of Art. 3 of the Federal Law of 08.11.2007 No. 257-FZ (hereinafter - the Platon board). The payment procedure for Platon is determined by Decree of the Government of the Russian Federation of June 14, 2013 No. 504 (hereinafter - the Rules).

Owners and owners of vehicles, the maximum permissible mass of which exceeds 12 tons, register them in a special register (paragraph 5, 38-55 of the Rules). The fee that is paid through the operator is indicated in the route map (paragraph 10 (1) of the Rules) or calculated by the operator in automatic mode using the data received from the device installed on the car (paragraph 7 of the Rules). Every day, the operator transfers to the federal budget income an amount that is determined as the amount of payments made by the owners for the routes traveled by vehicles (paragraph 16 of the Rules). Upon request, the payer can specify:

- amount of arrears on payment of the fee (subparagraph "a", paragraph 83 of the Rules);

- cash balance (paragraphs "b" p. 83 of the Rules);

- about operations on transfer by an operator to the federal budget income of the funds of the vehicle owner (owner) as a fee, depending on the path traveled by each vehicle (paragraph 84 of the Rules).

Accounting

Calculations of the transport tax are reflected in accounting on account 68 "Calculations of taxes and fees."

To do this, a sub-account "Settlements for transport tax" is opened to account 68. As a rule, the transport tax relates to expenses for ordinary activities (paragraph 5 of PBU 10/99). The order of its reflection in accounting depends on in which production or unit of the organization the vehicle for which the tax is charged is used.

Charge fee "Plato" is reflected in the following transactions:

- Dt 76 - Kt 51 - the advance payment to the operator is transferred (the basis is a payment or other document confirming the transfer).

- Dt 20 (44) - Kt 76 - the fare calculated in the Platon system is allocated to expenses (the basis is operator information on special request).

If it is stipulated by the accounting policy of the organization, you can additionally reflect the amount of the fee transferred by the operator to the budget: information on the transferred amounts can be obtained from the operator by special request. This operation is reflected in the subaccounts of account 76.

When calculating the transport tax, the following is posted:

- Dt 20 (23, 25, 26, 44) - Kt 68, subaccount "Calculations for transport tax" - accrued transport tax minus the fee "Platon", transferred to the budget by the operator.

Tax accounting

According to paragraph 2 of Art. 362 of the Tax Code of the Russian Federation, a taxpayer can reduce the amount of the transport tax calculated according to the results of the tax period in respect of each vehicle by the amount of the Platon payment calculated in the current period in relation to this vehicle, i.e. apply a deduction.

If the organization pays an advance payment to the operator without a route card, then only the amount that the operator credited to the budget can be taken to reduce the transport tax (letter of the Ministry of Finance of Russia dated 01/26/2017 No. 03-05-05-04 / 3747). This amount can be clarified by sending a request to the operator (paragraph 84 of the Rules).

The deduction is applied based on the results of the tax period, separately for each vehicle (paragraph 12, paragraph 2 of Article 362 of the Tax Code of the Russian Federation). If the Platon fee is greater than the amount of the transport tax, then the tax is not paid to the budget (paragraph 13, clause 2 of Article 362 of the Tax Code of the Russian Federation), and the portion of the Platon fee that exceeds the amount of the transport tax is taken into account in income tax expenses (paragraph 48.21, article 270 of the Tax Code of the Russian Federation).

If the amount of the transport tax is more than the Platon fee, then it is payable to the budget and in the amount of the paid amounts is included in income tax expenses (letter of the Ministry of Finance of Russia dated 06.09.2016 No. 03-05-05-04 / 52171).

In respect of all cars for which the Platon payment is made, advance payments for transport tax are not paid, even if established by regional law (paragraph 2 of paragraph 2 of Article 363 of the Tax Code of the Russian Federation).

For organizations that pay the Platon fee, the Federal Tax Service of Russia recommends already in 2016 to submit a transport tax declaration in a new form, approved by order of the Federal Tax Service of Russia dated 05.12.2016 No. MMV-7-21 / [email protected] (Letter of December 29, 2016 No. PA-4-21 / [email protected]).

In the program "1C: Accounting 8" To account for the Platon board, a special document called the Platon System Operator Report has been created, it is necessary to enter data on the transfer of the vehicle owner (owner) money to the federal budget as a fee, depending on the path traveled by each vehicle. The calculation of the amount of transport tax is carried out by the regulatory document with the type of operation "calculation of the transport tax".

Reduction of the transport tax on the Platon payment (the transport tax is higher than the Platon payment)

Example

OOO Furniture House owns a heavy truck (with a permitted maximum mass of over 12 tons) with an initial value of 6,608,000.00 rubles. (including 18% VAT - 1,008,000.00 rubles) for transporting goods to customers on public roads. The car is registered as a fixed asset.

Furniture House LLC is included in the register of the Platon system (hereinafter - the Platon board). In 2016, the tractor traveled 5,000 kilometers on federal roads; according to the results of the year, the amount of accrued transport tax turned out to be higher than the amount of the Platon payment transferred to the budget by the operator.

In accordance with the accounting policy, the organization applies in accounting PBU 18/02 "Accounting for calculations of corporate income tax."

Step by step instructions in the program "1C: Accounting 8" (rev. 3.0):

1. Down payment transfer to the operator

To perform the operation "Registration in the account of the transferred advance payment to the operator", you must first create a document Payment order, then, based on this document, enter the document "Write-off from the current account". As a result of the document "Write-off from the current account", the corresponding transactions will be generated.

If payment orders are created in the Client-Bank program, then it is not necessary to create them in 1C: Accounting 8. In this case, only the "Write-off from the current account" document is entered, which generates the necessary entries. The document "Write-off from the current account" can be created manually or on the basis of unloading from other external programs (for example, "Client-Bank").

After receiving the bank statement, in which the funds were debited from the current account, it is necessary to confirm the previously created document "Write-off from the current account" for the formation of transactions.

Menu: Bank and cash desk – Bank – Bank statements, document "Write-off from the current account".

In the document:

- In the "Settlement accounts" field, account 76.09 "Other settlements with different debtors and creditors" is automatically substituted.

- Check the filling of the remaining fields, as shown in Fig. 1.

- Check the box "Confirmed by bank statement".

- Button Hold and close.

To view the result of the document (Fig. 2), press the button DTKt

The debit of account 76.09 “Other Settlements with Various Debtors and Creditors” reflects the amount of the advance payment (replenishment of the account) to the operator of the state payment system “Platon” - LLC RT-Invest Transport Systems.

2. Reflection of the "Platon" board, transferred by the operator to the budget in the control unit and control unit

In order to carry out operations to reflect the Platon payment transferred by the operator to the budget in accounting and tax accounting, it is necessary to create a document Report of the system operator "Plato". In this document it is necessary to reflect the amount of the fee that the operator transferred to the budget - it can be found in the personal account of the organization from the report "Details on the personal account".

In order to make it possible to fill out this document, in the information register "Vehicle registration" (menu: Directories– Taxes– Transport tax– Vehicle Registration) it is necessary to put a checkmark "Registered in the registry of the Plato system (Fig. 3).

Creation of the document "Report of the operator of the Plato system (Fig. 4), menu: Shopping - Shopping - Plato System Operator Reportsbutton Create.

When filling out the document "Platon system operator report", indicate:

- In the “from” field - the date the expenses were reflected in the accounting records for the amount of the Platon fee transferred to the budget by the operator.

- In the field “Counterparty” - of the “Platon” payment collection operator - RT-Invest Transport Systems LLC.

- In the field "Contract" - the contract with the counterparty. Attention! The contract selection window displays only those contracts that have the type of contract "Other". On the hyperlink “Settlements” - settlement account 76.09 “Other settlements with different debtors and creditors”.

- In the tabular part of the document - the name of the vehicle, its state number and amount. The amount must be taken from the statement of the operator.

- Button Spend.

To view the result of the document "Report of the operator" Plato "(Fig. 5), click the button DTKt.

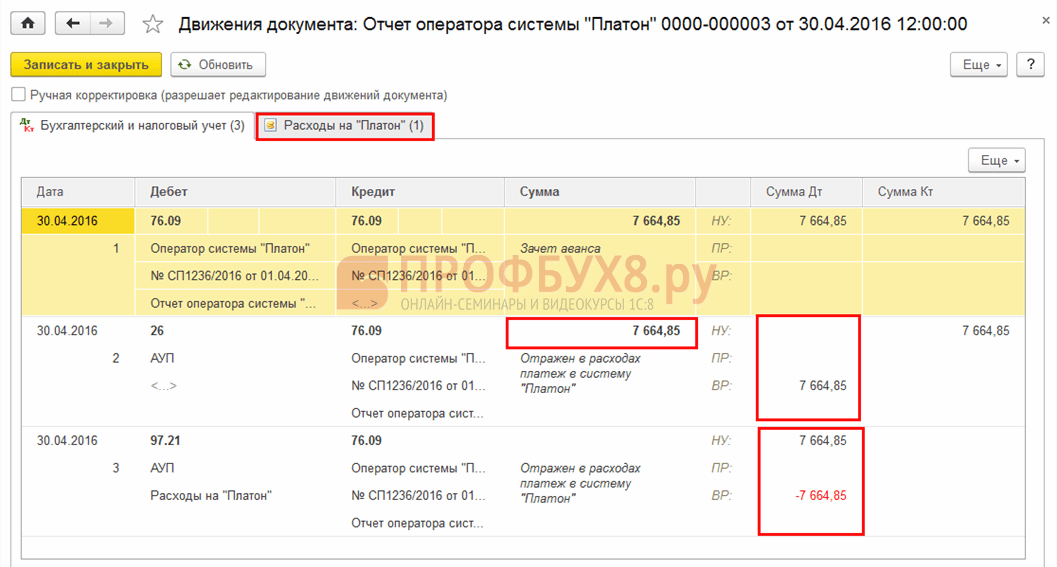

- Posting No. 1 - Set-off of the “Platon” fee transferred to the budget by the operator on account of the advance payment listed earlier. Since the Platon fee is paid in advance, when registering the Platon System Operator Report document in the program, the amounts previously paid are offset against the fee transferred by the operator to the budget.

- Posting No. 2 - Reflection in expenses of the amount of payment "Platon" (BU) - the amount of the payment transferred to the budget is reflected in the debit of the account for cost accounting. In our example, account 44.01 is used, which is set in the "Transport tax: ways of reflecting expenses" information register. Since in the income tax expenses the paid amount of the Platon fee will be taken into account only to the extent that it exceeds the amount of the paid transport tax for the year (paragraph 48.21 of article 270 of the Tax Code of the Russian Federation), a difference is formed (paragraph 8 of PBU 18/02 ), and since at the time of accounting for the Platon payment in accounting, it is not known how much it will be taken into account in tax accounting at the end of the year, this difference is temporary (paragraph 12 of PBU 18/02).

- Posting No. 3 - A technical transaction that reflects the amount of the Platon payment that the operator transferred to the budget in tax accounting for income tax calculations, namely, in order to reduce the amount of transport tax payable by the amount of the Platon payment transferred to the budget. Since this amount is only the estimated expense for income tax purposes and it will be finally determined only at the end of the year, it is accounted for in Dt 97.21 “Other deferred expenses”. It is this subaccount that is intended to automate the accounting of the excess of the Platon fee transferred to the budget over the amount of the accrued transport tax for the year. Simultaneously with the reflection of the estimated amount of expenditure in the NU, a temporary difference is formed, which will automatically close when the amount of the transport tax is determined minus the Platon fee transferred to the budget.

3. Calculation of the amount of transport tax

Before conducting operations to close the month, the accountant must fill out the form "Transport tax". For more information about filling out the "Transport tax" form, see the article "Acquisition and registration of a vehicle."

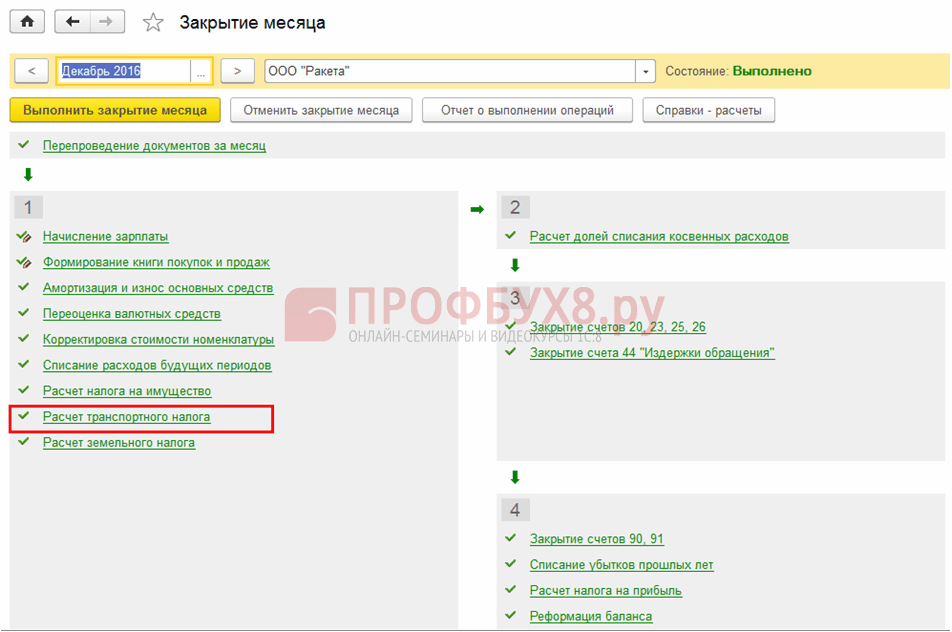

To calculate the amount of transport tax minus the paid amount of the fee "Plato" for the year, you must create a document Scheduled operation with the operation type "Calculation of transport tax" (Fig. 6). As a result of the creation of such a document, appropriate postings will be generated.

In our example, we will close all scheduled operations with a list for the month to see the calculation of the transport tax.

Execution of processing "Closing of the month" (Fig. 6), menu: Operations– Closing period– Closing month.

- Set the month that is closing.

- Before closing routine operations, it is necessary to restore the sequence of documents. To do this, click on the "Re-documenting for the month" hyperlink.

- To illustrate our example, select only the routine operation "Transport tax calculation".

To view the result of the document “Regulatory operation” with the operation type “Calculation of transport tax” (Fig. 7), press the button ДтКт.

The resulting postings reflect the following:

- Posting No. 1- reflection in the expenses of the amount of the transport tax minus the Platon fee - the posting shows the amount of the transport tax that is payable to the budget. This amount is calculated as follows: Tax base * Tax rate * Raising coefficient * Decreasing coefficient - The amount of the Platon payment transferred to the budget by the operator, where:

- The tax base (engine power) and the tax rate for the tractor, see fig. 3.

- Increasing coefficient \u003d 1, because the calculation is carried out for a truck (tractor), and not for a car.

- Decreasing coefficient \u003d 0.7500 (9 months / 12 months).

- The amount of the fee "Plato", transferred to the budget by the operator \u003d 7 650.00 rubles. (see fig. 5).

- The amount of transport tax payable to the budget is (456 hp * 45 rubles * 0.7500) - 7,650.00 rubles. \u003d 15,390.00 rubles. - 7 650,00 rub. \u003d 7 740 rub.

- Posting No. 2 - reflection of the permanent difference in the form of the Platon payment: since the Platon payment, taken into account as a possible expense, is less than the amount of the transport tax payable to the budget, it will not be taken into account in income tax expenses either this year or next. On the one hand, this leads to the reflection of a constant difference (paragraph 4 of PBU 18/02), and on the other, to the closing of the amounts taken into account as a possible expense under Dt 97.21 by posting Dt 44.01 Kt 97.21. At the same time, the temporary difference closes, which arose at the time the estimated amount was reflected in the tax account in the form of a Platon payment.

The decoding of the calculation of the transport tax can be found in the report "Help-calculation of the transport tax" (Fig. 8) (menu: Operations - Period End Closing - Reference Calculations).

4. Closing a cost accounting account

To perform the operation to close the cost accounting account, you must create a document Scheduled operationwith the operation type "Account closure 44" Costs of circulation "(Fig. 6). As a result of the creation of such a document, the corresponding transactions will be generated.

To view the result of the document “Scheduled operation” with the type of operation “Closing the account 44“ Costs of circulation ”(Fig. 9), press the button ДтКт.

The resulting postings mean the following:

- Posting No. 1 - cost accounting in the form of a “Platon” payment, transferred to the budget by the operator as part of financial results. Since the amount of the Platon fee is not taken into account for tax purposes (unless the amount of the fee is greater than the amount of tax), a constant difference is formed.

- Posting No. 2 - accounting of the amount of transport tax payable to the budget in accounting and tax accounting, as part of financial results.

- Posting No. 3 - accounting for the amount of accrued depreciation for the car as part of financial results.

5. Calculation of tax assets and liabilities

To perform the operation "Recognition of a permanent tax liability", you must create a document Scheduled operation with the type of operation "Calculation of income tax" (Fig. 6). As a result of the creation of this document, appropriate postings will be generated.

To view the result of the document “Regulatory operation” with the operation type “Calculation of income tax” (Fig. 10), press the button ДтКт.

Calculation of deferred taxes related to payment by the amount of the Platon fee transferred to the budget by the operator for 2016

Permanent tax liabilities recognized \u003d Platon fee amount transferred to the budget by the operator * Profit tax rate (1,530.00 rubles \u003d 7,650.00 rubles * 0.20).

A breakdown of the amount of deferred taxes can be found in the report “Help-calculation of tax assets and liabilities” (Fig. 11) (menu: Operations – Closing period – Reference calculations – Tax assets and liabilities).

6. Preparation of a transport tax declaration

To perform the operation "Preparation of a tax on transport tax", it is necessary to create a regulated report Transport tax declaration (annual).

Creation of the report "Declaration on the transport tax" (Fig. 12), menu: Reports – 1C-Reporting – Regulated Reports - button Create.

When filling out the document, indicate the following:

- In the opened form "Types of reports" - "Declaration on the transport tax (annual)".

- In the window that opens, in the field "Period" - 2016, in the field "Form Editing" - "dated 05.12.2016 No. MMV-7-21 / [email protected]".

- Button Create.

- Check the completion of the indicators of the title page ("Taxpayer", "Tax period (code)", "Reporting year", etc.), which are automatically filled with data contained in the information base. If any field is not filled, it is necessary to check the completeness of filling the infobase. The cells available for filling can be replenished manually.

- Button Fill. The calculation will automatically be filled with data on taxable items involved in the calculation for the reporting period.

- Using button Check – Check control ratios You can check the completion of the calculation. If errors are found during the verification, a warning window appears and a special window for navigating errors that need to be fixed.

- Button Write down.

Thus, for 2016, the calculated amount of the transport tax (that is, payable to the budget) for a heavy truck of the "Mercedes Benz Actros 1846LS Tractor" brand amounted to 7,740.00 rubles. At the same time, the amount of tax deduction calculated for travel in the Platon system is 7,650.00 rubles.

1C: ITS

For more information on the preparation of a transport tax declaration, see the section: “Reporting” - “Reporting in Programs” - “Transport Tax”.

When you purchase a vehicle and register it with the traffic police, the organization becomes a payer of transport tax (Article 357, Clause 1, Article 358 of the Tax Code of the Russian Federation).

Transport tax rates are determined by regional legislation, you can find them in the tax office at the place of registration of the vehicle. In this case, the base rates for transport tax are defined in Art. 361 of the Tax Code of the Russian Federation.

According to paragraph 1 of Art. 359 of the Tax Code of the Russian Federation the definition of the tax base depends on the type of vehicle.

When purchasing a truck, the organization pays tax based on the formula: Tax base * Tax rate * Decreasing coefficient, determined in accordance with paragraph 3 of Art. 362 of the Tax Code of the Russian Federation.

In addition, this formula also includes another indicator that reduces the amount of accrued transport tax - the payment for compensation for damage caused to roads, it is established by Part 5 of Art. 3 of the Federal Law of 08.11.2007 No. 257-FZ (hereinafter - the Platon board). The “Platon” fee collection procedure is determined by Decree of the Government of the Russian Federation dated June 14, 2013 No. 504 (hereinafter - the Rules).

Owners and owners of vehicles, the maximum permissible mass of which exceeds 12 tons, register them in a special register (paragraph 5, 38-55 of the Rules). The fee that is paid through the operator is indicated in the route map (paragraph 10 (1) of the Rules) or calculated by the operator in automatic mode using the data received from the device installed on the car (paragraph 7 of the Rules). Every day, the operator transfers to the federal budget income an amount that is determined as the amount of payments made by the owners for the routes traveled by vehicles (paragraph 16 of the Rules). Upon request, the payer can specify:

- amount of arrears on payment of the fee (paragraphs “a”, paragraph 83 of the Rules);

- cash balance (paragraphs “b”, paragraph 83 of the Rules);

- about operations on transfer by an operator to the federal budget income of the funds of the vehicle owner (owner) as a fee, depending on the path traveled by each vehicle (paragraph 84 of the Rules).

Accounting

Calculations of the transport tax are reflected in accounting on account 68 “Calculations of taxes and fees”.

For this, a sub-account “Settlements for transport tax” is opened to account 68. As a rule, the transport tax relates to expenses for ordinary activities (paragraph 5 of PBU 10/99). The order of its reflection in accounting depends on in which production or unit of the organization the vehicle for which the tax is charged is used.

Charge fee "Plato" is reflected in the following transactions:

- Dt 76 - Kt 51 - the advance payment to the operator is transferred (the basis is a payment or other document confirming the transfer).

- Dt 20 (44) - Kt 76 - the fare calculated in the Platon system is allocated to expenses (the basis is operator information on special request).

If it is stipulated by the accounting policy of the organization, you can additionally reflect the amount of the fee transferred by the operator to the budget: information on the transferred amounts can be obtained from the operator by special request. This operation is reflected in the subaccounts of account 76.

When calculating the transport tax, the following is posted:

- Dt 20 (23, 25, 26, 44) - Kt 68, subaccount "Calculations for transport tax" - the transport tax is calculated minus the fee "Platon" transferred to the budget by the operator.

Tax accounting

According to paragraph 2 of Art. 362 of the Tax Code of the Russian Federation, a taxpayer can reduce the amount of the transport tax calculated according to the results of the tax period in respect of each vehicle by the amount of the “Platon” fee calculated in the current period in relation to this vehicle, i.e. apply a deduction.

If the organization pays an advance payment to the operator without a route card, then only the amount that the operator credited to the budget can be taken to reduce the transport tax (letter of the Ministry of Finance of Russia dated 01/26/2017 No. 03-05-05-04 / 3747). This amount can be clarified by sending a request to the operator (paragraph 84 of the Rules).

The deduction is applied based on the results of the tax period, separately for each vehicle (paragraph 12, paragraph 2 of Article 362 of the Tax Code of the Russian Federation). If the Platon fee is greater than the amount of the transport tax, then the tax is not paid to the budget (paragraph 13, clause 2 of Article 362 of the Tax Code of the Russian Federation), and the portion of the Platon fee that exceeds the amount of the transport tax is taken into account in income tax expenses (paragraph 48.21, article 270 of the Tax Code of the Russian Federation).

If the amount of the transport tax is more than the Platon fee, then it is payable to the budget and in the amount of the paid amounts is included in income tax expenses (letter of the Ministry of Finance of Russia dated 06.09.2016 No. 03-05-05-04 / 52171).

In respect of all cars for which the Platon payment is made, advance payments for transport tax are not paid, even if established by regional law (para. 2 p. 2 of article 363 of the Tax Code of the Russian Federation).

For organizations that pay the Platon fee, the Federal Tax Service of Russia recommends for 2016 to submit a transport tax declaration in a new form, approved by order of the Federal Tax Service of Russia dated 05.12.2016 No. MMV-7-21 / [email protected] (Letter of December 29, 2016 No. PA-4-21 / [email protected]).

In the program “1C: Accounting 8 ″ To account for the Platon board, a special document, the Platon System Operator Report, was created. It is necessary to enter into it data on the transfer by the operator to the federal budget of the funds of the vehicle owner (owner) as a fee, depending on the path traveled by each vehicle. The calculation of the amount of transport tax is carried out by the regulatory document with the type of operation "calculation of the transport tax".

Reduction of the transport tax on the Platon payment (the transport tax is higher than the Platon payment)

Example

OOO Furniture House owns a heavy truck (with a permitted maximum weight of over 12 tons) with an initial cost of 6,608,000.00 rubles. (including 18% VAT - 1,008,000.00 rubles) for transporting goods to customers on public roads. The car is registered as a fixed asset.

Furniture House LLC is included in the Platon system registry (hereinafter - Platon board). In 2016, the tractor traveled 5,000 kilometers on federal roads; according to the results of the year, the amount of accrued transport tax was higher than the amount of the “Platon” fee transferred to the budget by the operator.

In accordance with the accounting policy, the organization applies in accounting PBU 18/02 “Accounting for the calculation of corporate income tax”.

Step-by-step instruction in the program “1C: Accounting 8 ″ (rev. 3.0):

1. Down payment transfer to the operator

To perform the operation "Registration in the account of the transferred advance payment to the operator", you must first create a document Payment order, then, based on this document, enter the document "Write-off from the current account". As a result of the document “Write-off from the current account", the corresponding transactions will be generated.

If payment orders are created in the Client-Bank program, then it is not necessary to create them in 1C: Accounting 8 ″. In this case, only the “Write-off from the current account” document is entered, which generates the necessary entries. The document "Write-off from the current account" can be created manually or on the basis of unloading from other external programs (for example, "Client-bank").

After receiving the bank statement, in which the funds were debited from the current account, it is necessary to confirm the previously created document "Write-off from the current account" for the formation of transactions.

Menu: Bank and cash desk – Bank – Bank statements, document "Write-off from the current account".

In the document:

- In the field “Settlement accounts”, account 76.09 “Other settlements with different debtors and creditors” is automatically substituted.

- Check the filling of the remaining fields, as shown in Fig. 1.

- Check the box “Confirmed by bank statement”.

- Button Hold and close.

To view the result of the document (Fig. 2), press the button DTKt

The debit of account 76.09 “Other Settlements with Various Debtors and Creditors” reflects the amount of the advance payment (replenishment of the account) to the operator of the state payment system “Platon” - LLC RT-Invest Transport Systems.

2. Reflection of the “Platon” board, transferred by the operator to the budget in the control unit and control unit

In order to carry out operations to reflect the Platon payment transferred by the operator to the budget in accounting and tax accounting, it is necessary to create a document Report of the Platon system operator. In this document it is necessary to reflect the amount of the fee that the operator transferred to the budget - it can be found in the personal account of the organization from the report “Details on the personal account”.

In order to make it possible to fill out this document, in the “Vehicle Registration” information register (menu: Directories– Taxes– Transport tax– Vehicle Registration) it is necessary to put a checkmark “Registered in the registry of the Plato system” (Fig. 3).

Creation of the document “Report of the operator of the Platon system (Fig. 4), menu: Shopping - Shopping - Reports of the Platon system operatorbutton Create.

When filling out the document “Report of the operator of the Platon system, indicate:

- In the “from” field - the date the expenses were reflected in accounting for the amount of the “Platon” fee transferred to the budget by the operator.

- In the field “Counterparty” - of the charging operator “Platon” - LLC RT-Invest Transport Systems.

- In the field “Contract” - the contract with the counterparty. Attention! The contract selection window displays only those contracts that have the type of contract “Other”. On the hyperlink “Settlements” - settlement account 76.09 “Other settlements with different debtors and creditors”.

- In the tabular part of the document - the name of the vehicle, its state number and amount. The amount must be taken from the statement of the operator.

- Button Spend.

To view the result of holding the document “Platon System Operator Report” (Fig. 5), press the DTKt button.

- Posting No. 1 - Set-off of the “Platon” fee, transferred to the budget by the operator on account of the advance payment listed earlier. Since the Platon fee is paid in advance, when registering the Platon System Operator Report document in the program, the previously paid amounts are set off against the fee transferred by the operator to the budget.

- Posting No. 2 - Reflection in expenses of the amount of payment “Platon” (BU) - the amount of the payment transferred to the budget is reflected in the debit of the expense account. In our example, account 44.01 is used, which is set in the information register “Transport tax: ways to reflect expenses”. Since the amount of the Platon fee paid in profit tax expenses will be taken into account only to the extent that it exceeds the amount of the paid transport tax for the year (paragraph 48.21 of article 270 of the Tax Code of the Russian Federation), a difference is formed (paragraph 8 of PBU 18/02 ), and since at the time of accounting for the Platon payment in accounting, it is not known how much it will be taken into account in tax accounting at the end of the year, this difference is temporary (paragraph 12 of PBU 18/02).

- Posting No. 3 - A technical entry that reflects the amount of the Platon fee transferred to the budget by the operator in the tax accounting for income tax calculations, namely, in order to reduce the amount of transport tax payable by the amount of the Platon fee transferred to the budget. Since this amount is only the estimated expense for the purpose of income tax and it will be finally determined only at the end of the year, it is accounted for in Dt 97.21 “Other deferred expenses”. It is this subaccount that is intended to automate the accounting of the excess of the Platon fee transferred to the budget over the amount of accrued transport tax for the year. Simultaneously with the reflection of the estimated amount of expenditure in the NU, a temporary difference is formed, which will automatically close when the amount of the transport tax is determined minus the Platon fee transferred to the budget.

3. Calculation of the amount of transport tax

Before conducting operations to close the month, the accountant must fill out the form “Transport tax”. For more information about filling out the “Transport tax” form, see the article “Acquisition and registration of a vehicle”.

To calculate the amount of transport tax minus the paid amount of the fee "Plato" for the year, you must create a document Scheduled operation with the operation type “Calculation of transport tax” (Fig. 6). As a result of the creation of such a document, appropriate postings will be generated.

In our example, we will close all scheduled operations with a list for the month to see the calculation of the transport tax.

Execution of processing “Closing of the month” (Fig. 6), menu: Operations– Closing period– Closing month.

- Set the month that is closing.

- Before closing routine operations, it is necessary to restore the sequence of documents. To do this, click on the “Re-documenting per month” hyperlink.

- To illustrate our example, select only the routine operation “Transport Tax Calculation”.

To view the result of the document “Regulatory operation” with the operation type “Calculation of transport tax” (Fig. 7), press the button ДтКт.

The resulting postings reflect the following:

- Posting No. 1- reflection in the expenses of the amount of the transport tax minus the “Platon” fee - the posting shows the amount of the transport tax that is payable to the budget. This amount is calculated as follows: Tax base * Tax rate * Raising coefficient * Decreasing coefficient - The amount of the Platon payment transferred to the budget by the operator, where:

- The tax base (engine power) and the tax rate for the tractor, see fig. 3.

- Increasing coefficient \u003d 1, because the calculation is carried out for a truck (tractor), and not for a car.

- Decreasing coefficient \u003d 0.7500 (9 months / 12 months).

- The amount of payment "Platon", transferred to the budget by the operator \u003d 7 650.00 rubles. (see fig. 5).

- The amount of transport tax payable to the budget is (456 hp * 45 rubles * 0.7500) - 7,650.00 rubles. \u003d 15,390.00 rubles. - 7 650,00 rub. \u003d 7 740 rub.

- Posting No. 2 - reflection of the permanent difference in the form of the Platon fee: since the Platon fee, taken into account as a possible expense, is less than the amount of the transport tax payable to the budget, it will not be included in income tax expenses either this year or next. On the one hand, this leads to the reflection of a constant difference (paragraph 4 of PBU 18/02), and on the other, to the closing of the amounts taken into account as a possible expense under Dt 97.21 by posting Dt 44.01 Kt 97.21. At the same time, the temporary difference closes, which arose at the time the estimated amount was reflected in the tax accounting in the form of a Platon payment.

The decoding of the calculation of the transport tax can be found in the report “Help-calculation of the transport tax” (Fig. 8) (menu: Operations - Period End Closing - Reference Calculations).

4. Closing a cost accounting account

To perform the operation to close the cost accounting account, you must create a document Scheduled operationwith the operation type “Account closure 44“ Costs of circulation ”(Fig. 6). As a result of the creation of such a document, appropriate postings will be generated.

To view the result of the document “Scheduled Operation” with the type of operation “Closing Account 44“ Circulation Costs ”(Fig. 9), press the DTKt button.

The resulting postings mean the following:

- Posting No. 1 - cost accounting in the form of a “Platon” fee, transferred to the budget by the operator as part of financial results. Since the amount of the Platon fee is not taken into account for tax purposes (unless the amount of the fee is greater than the amount of tax), a permanent difference is formed.

- Posting No. 2 - accounting of the amount of transport tax payable to the budget in accounting and tax accounting, as part of financial results.

- Posting No. 3 - accounting for the amount of accrued depreciation for the car as part of financial results.

5. Calculation of tax assets and liabilities

To perform the operation “Recognition of a permanent tax liability”, you must create a document Scheduled operation with the type of operation “Calculation of income tax” (Fig. 6). As a result of the creation of this document, appropriate postings will be generated.

To view the result of the document “Regulatory operation” with the operation type “Calculation of income tax” (Fig. 10), press the button ДтКт.

Calculation of deferred taxes related to payment by the amount of the Platon fee transferred to the budget by the operator for 2016

Permanent tax liabilities recognized \u003d Platon payment amount transferred to the budget by the operator * Profit tax rate (1,530.00 rubles \u003d 7,650.00 rubles * 0.20).

A breakdown of the amount of deferred taxes can be found in the report “Help-calculation of tax assets and liabilities” (Fig. 11) (menu: Operations – Closing period – Reference calculations – Tax assets and liabilities).

6. Preparation of a transport tax declaration

To perform the operation “Preparation of a tax on transport tax” it is necessary to create a regulated report Transport tax declaration (annual).

Creation of the report “Declaration on transport tax” (Fig. 12), menu: Reports – 1C-Reporting – Regulated Reports - button Create.

When filling out the document, indicate the following:

- In the opened form “Types of reports” - “Declaration on the transport tax (annual)”.

- In the window that opens, in the "Period" field - 2016, in the "Form revision" field - "dated 05.12.2016 No. MMV-7-21 / [email protected]».

- Button Create.

- Check the filling of the indicators of the title page (“Taxpayer”, “Tax period (code)”, “Reporting year”, etc.), which are automatically filled with data contained in the information base. If any field is not filled, it is necessary to check the completeness of filling the infobase. The cells available for filling can be replenished manually.

- Button Fill. The calculation will automatically be filled with data on taxable items involved in the calculation for the reporting period.

- Using button Check – Check control ratios You can check the completion of the calculation. If errors are found during the verification, a warning window appears and a special window for navigating errors that need to be fixed.

- Button Write down.

Thus, for 2016, the calculated amount of transport tax (that is, payable to the budget) for a heavy truck of the “Mercedes Benz Actros 1846LS Tractor” brand amounted to 7,740.00 rubles. At the same time, the amount of tax deduction calculated for travel in the Platon system is 7,650.00 rubles.

By default, an entry is entered in this register for the allocation of tax amounts (advance tax payments) for all vehicles to the debit of account 26 “General expenses” under the item of expenses Property taxes. If this method of reflection corresponds to the method enshrined in the accounting policies of the organization, then for its use it is enough to indicate the unit to which the expenses relate. If the accounting policy provides for a different account for accounting for transport tax expenses, you can make changes to the existing record, or enter a new record in the register with a later validity date.

Calculation of the transport tax, taking into account the fee on the Platon system in 1s 8.3

Preparation of a transport tax declaration In order to complete the operation “Preparation of a transport tax declaration”, it is necessary to create a regulated report Transport tax declaration (annual). Creation of the report "Declaration on the transport tax" (Fig.

12), menu: Reports - 1C-Reporting - Regulated reports - Create button. When filling out the document, indicate the following:

- In the opened form “Types of reports” - “Declaration on the transport tax (annual)”.

- In the window that opens, in the "Period" field - 2016, in the "Form revision" field - "dated 05.12.2016 No. MMV-7-21 /".

- Create button.

- Check the filling of the indicators of the title page (“Taxpayer”, “Tax period (code)”, “Reporting year”, etc.), which are automatically filled with data contained in the information base.

1s: franchisee accountant consultant

As a result of the creation of this document, appropriate postings will be generated. To view the result of the document “Regulatory operation” with the type of operation “Calculation of income tax” (Fig.

10) press the DTKt button. Fig. 10 Calculation of deferred taxes related to payment by the amount of the Platon payment transferred to the budget by the operator for 2016. Permanent tax liabilities are recognized \u003d The amount of the Platon payment transferred to the budget by the operator * Income tax rate (1,530.00 rub.

\u003d 7,650.00 rubles. * 0.20). A breakdown of the amount of deferred taxes can be found in the report “Help-calculation of tax assets and liabilities” (Fig. 11) (menu: Operations - Closing the period - Help-calculations-Tax assets and liabilities). Fig. 11 6.

Plato in the transport tax declaration

In order to make it possible to fill out this document, in the “Vehicle Registration” information register (menu: Directories - Taxes - Transport tax - Vehicle registration), you must select the “Registered in the Platon” system registry (Fig. 3). Fig.3 Creation of the document "Report of the operator of the Platon system (Fig.

4), menu:

Info

Shopping - Shopping - Reports of the Platon system operator, Create button. When filling out the document “Report of the operator of the Platon system, indicate:

- In the “from” field - the date the expenses were reflected in accounting for the amount of the “Platon” fee transferred to the budget by the operator.

- In the field “Counterparty” - of the charging operator “Platon” - LLC RT-Invest Transport Systems.

- In the field “Contract” - the contract with the counterparty.

Attention! The contract selection window displays only those contracts that have the type of contract “Other”.

Setting up an account and cost analytics for plato in 1s: accounting 8

- Pull and close button. Fig. 1 To view the result of the document (Fig. 2), press the button ДТКт Fig. 2 According to the debit of account 76.09 “Other settlements with different debtors and creditors” the amount of the advance payment (top-up) to the operator of the state payment system “Platon” - LLC is reflected RT-Invest Transport Systems. 2. Reflection of the Platon payment transferred by the operator to the budget in the accounting and tax authorities. To carry out the operations on the reflection of the Platon payment transferred by the operator to the budget in accounting and tax accounting, it is necessary to create the Platon system operator report document.

Check the box “Confirmed by bank statement”.

In this document it is necessary to reflect the amount of the fee that the operator transferred to the budget - it can be found in the personal account of the organization from the report “Details on the personal account”.

Plato System Operator Report

Tax Code of the Russian Federation), and the portion of the Platon payment that exceeds the amount of the transport tax is taken into account in income tax expenses (Section 48.21, Article 270 of the Tax Code of the Russian Federation). If the amount of the transport tax is more than the Platon fee, then it is payable to the budget and in the amount of the paid amounts is included in income tax expenses (letter of the Ministry of Finance of Russia dated 06.09.2016 No. 03-05-05-04 / 52171).

Attention

In respect of all cars for which the Platon payment is made, advance payments for transport tax are not paid, even if established by regional law (para. 2 p. 2 of article 363 of the Tax Code of the Russian Federation). For organizations that pay the Platon fee, the Federal Tax Service of Russia recommends already in 2016 to submit a transport tax declaration in the new form approved by order of the Federal Tax Service of Russia dated 05.12.2016 No. MMV-7-21 / (letter dated 29.12.2016 No. PA-4 -21 /).

Since this amount is only the estimated expense for the purpose of income tax and it will be finally determined only at the end of the year, it is accounted for in Dt 97.21 “Other deferred expenses”. It is this subaccount that is intended to automate the accounting of the excess of the Platon fee transferred to the budget over the amount of accrued transport tax for the year.

Simultaneously with the reflection of the estimated amount of expenditure in the NU, a temporary difference is formed, which will automatically close when the amount of the transport tax is determined minus the Platon fee transferred to the budget. 3. Calculation of the amount of transport tax Before conducting operations to close the month, the accountant must fill out the form “Transport tax”.

For more information about filling out the “Transport tax” form, see the article “Acquisition and registration of a vehicle”.

The question is - will they be? Aleksey 5 - 07/14/17 - 05:21 (4) If only they change the Tax Code, not earlier than Aleksey 6 - 07/14/17 - 05:27 The document is intended to reduce the amount of transport tax. Moreover, according to 362 of the Tax Code of the Russian Federation 1. Taxpayers-organizations calculate the amount of tax and the amount of advance payment of tax on their own. The amount of tax payable by taxpayers - individuals is calculated by the tax authorities on the basis of information that is submitted to the tax authorities by the bodies that carry out state registration of vehicles on the territory of the Russian Federation. Those.

Filling out the transport tax declaration

- 3 Reflection of the fee in the costs taken into account in the calculation of income tax (OSNO)

- 4 Reflection of fees in the costs taken into account when calculating the single tax (STS)

Tax accounting of transactions related to payments to the Platon system Since 2016, taxpayers paying a fee to the Platon system in relation to “heavy trucks” with a carrying capacity of more than 12 tons have the right to reduce the transport tax for each vehicle by the amount of the payment for this vehicle for the tax period (paragraph 12, paragraph 1 of article 362 of the Tax Code). The excess of the specified fee over the transport tax is recognized as an expense and reduces the income tax for the tax (reporting) period (subparagraph 49 of paragraph 1 of article 264, paragraph 48.21 of article 270 of the Tax Code of the Russian Federation).

The same procedure is provided for with respect to the single tax at the simplified tax system (clause 37 of clause 1 of article 346.16 of the Tax Code).

An individual entrepreneur who equates to a physicist needs to apply for a tax exemption to the tax authorities, but the LLC considers the tax independently, and accordingly reflects the data on the payment of Plato in the program through this document Two Plus Two 7 - 07/14/17 - 06:41 (4) I mean, are you not friends with the debugger? You have a demobase where everything works and yours where it does not work. And the debugger does not help out? Aleksey 8 - 07/14/17 - 06:47 (7) In the demo version it also does not work with IP. orangekrs 9 - 07/18/17 - 05:49 (7) No, I have a demobase where it does not work and there is mine, where it does not work either. And yes, when in the debugger the jumps across all 100,500 BSP modules are a little less than it does not give an answer why.

The help-calculation of the transport tax in 1C 8.3 is the result of the regulatory operation "Calculation of the transport tax" and can be used as a tax register for the transport tax. The form is available in the section Operations - Closing of the month and can be generated from the routine operation Calculation of the transport tax or from the list of References - calculations: Step 5. Filling out the transport tax declaration The calculated tax with deduction is reflected in the transport tax declaration in the new form approved by the Order Federal Tax Service of Russia dated 05.12.2016 No.MMV-7-21 / 668: Reflection of fees in expenses taken into account when calculating income tax (OSNO) If the fee to the Platon system is greater than the calculated tax, then the excess amount can be to take into account in expenses when calculating income tax (paragraph 49, paragraph 1, article 264, paragraph 48.21, article 270 of the Tax Code of the Russian Federation) or the single tax with the simplified tax system, (paragraph 37, paragraph 1, article 346.16 of the Tax Code )

On November 15, 2015, the Platon system began to operate, with the help of which the state levies a fee on trucks with a permitted mass of more than 12 tons for causing damage to public roads. Only the lazy did not have time to speculate about the fairness of such a "tax" and about the adequacy of the fare. However, few people still know what to do after they have paid for the "fare." For example, how to reflect these costs in accounting and tax accounting? About this in his article will tell the financial consultant of the company "Finguru" Elena Krokhmal.

Accounting

The charging system provides two ways to calculate fees:

Route map. A one-time Route Card is issued in the Personal Account, Mobile Application or the User Information Support Center.

On-board device. The use of the on-board device for calculating the board is carried out in automatic mode - inside there is a GSM / GPRS communication module, as well as a GLONASS / GPS navigation module.

If everything is relatively simple with the route map, then you will have to tinker with the on-board device before using it for the first time - first you need to capitalize it by reflecting it on the off-balance account and appointing a materially responsible person.

After you have made the journey and paid a fee, the costs must be recorded in your bookkeeping. Reliable data on expenses for a given period can be obtained using the printout of the Detail Report from the operator’s personal account. This document will be a confirmation of the fact of the route of a particular truck.

Moreover, this detailing is mandatory for taxpayers who apply the General taxation system, because these expenses reduce taxable profit.

For taxpayers on the simplified tax system (income minus expenses) this listing is also necessary. Although they cannot take these costs into account in expenses, the details will confirm the legitimacy of debiting funds from the current account to pay for Platon services.

Reflect the device on the off-balance account as follows:

015 "On-board device of the Plato system":

Or at the cost specified in the contract for gratuitous use;

Or in a conditional assessment (for example, 1 rub.).

Accounting of expenses of the Platon system is carried out using a separate sub-account, for example, "Calculations on the fare of a truck on federal highways," open to the account:

76 "Settlements with various debtors and creditors."

The advance transferred to the operator is reflected at the debit of the specified subaccount.

After the operator deducts the fee from the personal account of the organization, it is necessary to reflect the expense of the debit of the account:

Or 20 "Main production" - for transport companies;

Or 44 "Costs to sell" - for trading companies that deliver the goods to the buyer on their own.

Tax accounting

Tax accounting of travel expenses as a part of expenses differs for taxpayers using the General Taxation System (EITI), from taxpayers using the simplified tax system (income minus expenses).

Confirm expenses under the General system of taxation is necessary by listing from the personal account of the system.

Source: Letter of the Ministry of Finance dated 01/11/2016 No. 03-03-RZ / 64

In the detailed report of the Plato operator, you will see data on the route of a particular truck with reference to the start and end times of the movement and information about the amount of the toll deducted from the personal account of the organization. Based on these data, the amount paid can be included in other expenses.

Not be superfluous to assure the printout with the signature of an accountant.

In addition, a trip sheet must be attached to the printed report to confirm the business orientation of the trip.

Attention. The lack of primary accounting documents not only serves as a basis for refusing to recognize the expenses incurred in order to calculate income tax, but also forms an independent type of tax violation.

The organization may be fined by the IFTS if it finds during the tax audit the absence of primary documents or accounting registers. The minimum fine is 10,000 rubles. A fine in this amount can be imposed in the absence of primary documents confirming the costs, although these costs are reflected in the costs in accounting (paragraph 1 of article 120 of the Tax Code of the Russian Federation).

Learning environment: new projects A typical project of a school with 825 seats

A catalog of typical projects of social infrastructure buildings has been created in the Moscow region

A catalog of typical projects of social infrastructure buildings has been created in the Moscow region

Turnkey Cottage Construction Roadmap

The report of the head of the Ministry of Construction of Russia Mikhail I at a meeting of the Commission under the President of the Russian Federation on monitoring the achievement of targets of socio-economic development