The transfer of wages to employees should be made 2 times a month - in advance and in the main payment. But sometimes the company has financial difficulties in which the accrual was made, but there were no payments. How to fill in 6 personal income tax if the salary of employees is accrued but not paid? Let's consider this situation with examples.

Introduction

How to reflect in the declaration a difficult financial situation for the organization, if the salary was accrued, but not paid. How to indicate the accrual of income and personal income tax in the calculation, and is it necessary to fill out section 2 for this situation?

Filling out the report is regulated in the Tax Code Art. 230 p. 2. All business entities that acted as tax agents in the calendar year are required to submit 6 personal income tax if at least in one period there was an accrual of earnings and taxes. Quarters 1, 2, 3, 4 are considered reporting. At the same time, the deadlines for the submission of declarations are clearly defined.

Section 1 must be completed on an accrual basis. In the second, information is entered in the reporting period when payments were made.

In the case of payroll in one quarter, and transfers in another, the information in the declaration should be reflected after completion. This applies to the situation when there was a salary delay.

For example, wages are accrued on March 5, the tax is withheld on March 6. This should be reflected in the report for 1 quarter in the first section.

Tax agents miss the moment of filling out the second section. In this case, the transfer of salaries to individuals was made in the 2nd quarter. In the form, in the 2nd part, you need to reflect the transfer of previously accrued income for the 1st quarter.

The Tax Code clearly defines that the last date of the month in which income was accrued is recognized as the day of receipt of remuneration. In this case, the enumeration may not be made.

According to the Tax Code, agents are required to withhold personal income tax from the accrued wages at the time of transfer. The tax must be transferred no later than the next business day. This applies not only to salaries, but also to sick leave and vacation sheets.

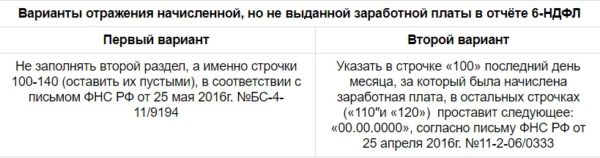

Reporting for this situation must be generated, while you need to fill out only the data of section 1 in relation to accrued wages. In the lines to reflect taxes, you must put zeros.

What will the employer face if income is not paid on time

The right to timely pay income to employees is enshrined in the following acts:

- In the Labor Code of the Russian Federation;

- in a collective agreement;

- in the internal documents of the organization;

- in labor contracts with employees.

If there were no income payments, questions may arise not only from the tax service in the absence of payments, but also from labor inspectors.

Employees have the right to refuse work after prior notice to the employer due to delayed wages within 2 weeks from the due date of payment. This right is enshrined in the Labor Code Art. 142. If employees exercise this possibility, the employer will be obliged to reimburse them for the average wage for each day in parts or in full until the debt is paid off.

In addition, employees will need to be compensated for the payment of wages with a delay, which is calculated at the rate of the Bank of the Russian Federation.

The employer will be fined for violation of Art. 5.27 AK. In case of failure to take measures to repay the debt, criminal punishment is possible in accordance with the Criminal Code, paragraph 1 of Art. 145.

Filling must be performed on an accrual basis from the beginning of the year in reports for the first 3 months, 1-2 quarter, 1-3 quarter and for the year:

- Line 070 reflects the total amount of personal income tax withheld as of the date of submission of the calculation in the total amount;

- In line 080, it is necessary to enter the amount of taxes not withheld on the date of submission of the declaration from the beginning of the calendar year. This rule is regulated in the Tax Code Art. 226 para. 5 and art. 226.1 item 14.

If the salary accrued for January - March was paid only in April, and personal income tax was withheld when transferring funds to employees in April, zeros should be entered in lines 070 and 080 for the 1st quarter.

In the half-year report, the amount of tax withheld should be included in line 070.

The reflection of the deposited salary accrued for the 1st quarter and the taxes calculated from it are included in lines 020 and 040 in the report for both the quarter and the half year.

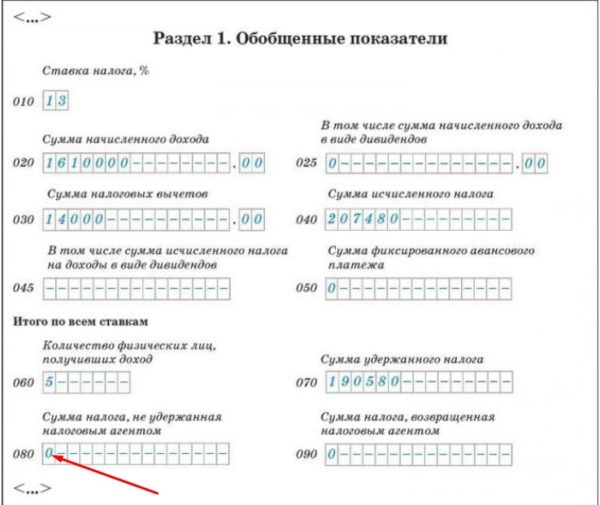

Sample filling 1 section:

The data for the second section of form 6 of the personal income tax should be reflected when the company pays the salary, in that reporting period. For the situation described above, income was transferred only in April, which means that section 2 should be filled out only in the half-year report.

These positions are regulated in the Tax Code:

- For p. 100 - art. 223;

- for p. 110 - Art. 226 para. 4 and art. 226.1. item 7;

- for p. 120 - Art. 226 para. 6 and art. 226.1. item 9.

An example of registration of 6 personal income tax in case of non-payment of wages

The organization is going through difficult financial times. Wages in the current year are accrued on time during January-May, but payments are delayed. In June, the employer began to pay off debts to the staff. The final payment was made on June 25, at the same time the tax was transferred. In subsequent periods, the accrual and transfer of taxes and wages were made on time. Salary was accrued on the last day of the month, transfer - on the first working day of the next.

In this case, is it necessary to submit a calculation of 6 personal income tax for 1 quarter? And how to fill out a declaration for half a year?

The monthly wage fund is 100.00 thousand rubles. Accordingly, for 6 months the income is 600.00 thousand rubles. There are no deductions, personal income tax is calculated only at 13%.

Filling in 6 personal income tax with a delay in the payment of wages for the 1st quarter is as follows:

- 010 - tax rate 13%;

- 020 - wage fund for three months 300,000;

- 040 - the amount of calculated personal income tax 39,000;

- 070 – 140 – 0.

An example of filling out a report for the 1st half of the year:

- 010 - tax rate 13%;

- 020 - wage fund for six months 600,000;

- 030 - no deductions applied 0;

- 040 - the amount of calculated tax for 6 months 78,000;

- 070 - the amount of tax withheld for 5 months 65,000;

- 100 –

| 31.01.2017 | 28.02.2017 | 31.03.2017 | 30.04.2017 | 31.05.2017 |

- 110 –

| 25.06.2017 | 25.06.2017 | 25.06.2017 | 25.06.2017 | 25.06.2017 |

- 120 –

| 26.06.2017 | 26.06.2017 | 26.06.2017 | 26.06.2017 | 26.06.2017 |

- 130 –

| 100000 | 100000 | 100000 | 100000 | 100000 |

- 140 –

| 13000 | 13000 | 13000 | 13000 | 13000 |

Formation of the report for 9 months and for the year is carried out in the usual manner.

In the case of unpaid income, when making a declaration, it is important to fill in lines 070 and 080, where data on actually withheld or not withheld personal income tax should be entered.

If January salary was paid in the next month and further all calculations were made on time, the form is filled out in the usual way.

Conclusion

Late payment of wages due to the fault of the employer can cause not only fines and sanctions from the tax authorities and labor inspectorates, but also certain difficulties for accountants, how to reflect the accrued salary in 6 personal income tax. When drawing up the calculation, it is important to reflect information in a timely manner, if necessary, on line 080 and fill out section 2, taking into account the repayment of debt.

Transfer of losses to the future in 1C: Accounting 8

Sample certificate of no debt

Issuance of money for a business trip in cash and on a card

payroll taxes

Preferential pension: who is entitled, how to get