Good day. Please clarify the expense item money for drawing up a REPORT ON THE CASH FLOWS on the payment of fines and penalties for taxes assessed in the framework of the exit tax audit.

Penalties paid to the budget are included in the line Other payments on current operations (4125).

The rationale for this position is given below in the materials of the General Accountant System

Reflect fines for tax offenses and penalties in accounting as part of tax sanctions. When calculating income tax, do not take into account fines and penalties.

Tax legislation separates the concepts of “penalty” and “fine”. Penalties are the amount of money that the organization must transfer to the budget in case of untimely fulfillment of the obligation to pay tax (paragraph 1 of article 75 of the Tax Code of the Russian Federation). The penalty is a tax sanction, which is levied on the organization for the permitted tax offense (Article 114 of the Tax Code of the Russian Federation). The sizes of fines for tax offenses are given in the table.

For accounting purposes, fines and penalties can be combined into one category of accounting objects - tax sanctions. This approach does not contradict the objectives of accounting, in particular, providing complete and reliable information about the organization’s activities and the basic principles of its management - rationality and priority of content over the form (paragraph 1 of article 13 of the Law of December 6, 2011 No. 402-FZ, paragraph 10 Accounting and Reporting Regulations).

The amount of accrued tax sanctions does not form a contingent income tax expense (, paragraph 20 of PBU 18/02). Therefore, in accounting, reflect these amounts directly on account 99 “Profit and loss” in correspondence with account 68 “Calculations for taxes and fees” (“Calculations for social insurance and security ”). To provide analytical accounting of tax sanctions on accounts, it is advisable to open subaccounts with a breakdown of taxes on which sanctions have been accrued (for example, the subaccount “Penalties (interest) on income tax”).

The calculation of tax sanctions reflect the posting:

Debit 99 Credit 68 (69) sub-account “Fines (penalties)”

- A fine has been charged for a tax violation (penalties for arrears). *

When calculating income tax, the organization is not entitled to take into account the amount of fines and penalties (paragraph 2 of article 270 of the Tax Code of the Russian Federation).

An example of reflection in accounting and taxation of tax sanctions (penalties and fines)

According to the results of six months, the following data are reflected in the Alpha accounting:

- on a loan of subaccount 90-1 - revenue from sales in the amount of 11.8 million rubles;

- on the debit of subaccount 90-2 - the cost of goods sold in the amount of 7 500 000 rubles .;

- according to the debit of subaccount 90-3 - VAT from sales proceeds in the amount of 1,800,000 rubles.

In June, according to the results of the tax audit of the organization, interest was charged in the amount of 200,000 rubles. and a fine of 250,000 rubles. income tax.

When closing the reporting period in accounting, the financial result is formed:

Debit 90-9 Credit 99 sub-account “Profit (loss) before tax”

- 2 500 000 rub. (11,800,000 rubles. - 1,800,000 rubles. - 7,500,000 rubles.) - reflects profit from sales for six months;

Debit 99 subaccount "Contingent expense for income tax" Credit 68 subaccount "Calculations for income tax"

- 500,000 rubles. (2,500,000 rubles.? 20%) - the amount of the contingent expense for income tax has been accrued.

The amount of tax sanctions in the formation of the financial result was not taken into account. Accrual of sanctions accountant reflected the posting:

Debit 99 Credit 68 sub-account “Penalties (interest) on income tax”

- 450,000 rubles. - accrued fines and penalties for income tax.

In the balance sheet, the amount of tax sanctions is involved in the formation of the indicator of line 1370 “Retained earnings (uncovered loss)” (paragraph 83 of the Regulation on Accounting and Reporting). In the Report on financial results the amount of sanctions can be reflected in line 2460 “Other”.

The statement of financial results regarding the formation of calculations for profit tax and net profit (loss) of Alfa’s accountant was as follows:

|

Title of report items |

String Codes |

For six months, rub. |

|

Profit (loss) before tax |

||

|

Current income tax |

||

|

Pending change tax liabilities |

||

|

Pending change tax assets |

Credit turnover on accounts 50, 51, 52, 55 in correspondence with accounts 57 “Transfers on the way”, 68 “Calculations on taxes and fees” (excluding the sub-account “Calculations on income tax”), 69 “Calculations on social insurance and collateral ”, 71“ Settlements with accountable persons ”, 73“ Settlements with personnel for other operations ”, 76“ Settlements with various debtors and creditors ”, 91-2“ Other expenses ”* |

|

The statement of cash flows (ODDS) is part of the annual accounting. This report is not the first time accountants have submitted this report. Therefore, we dwell only on those features of its filling that cause difficulties.

We show the VAT movement separately and collapsed

All receipts to the organization and all amounts transferred to counterparties must be “cleared” of VAT before filling out the report sub. “B” p. 16 PBU 23/2011. Some accountants may have difficulty with this. After all, we are talking about the movement of money in which VAT is “sitting”. And in accounting, the payment / receipt of VAT as part of such payments is not always separately reflected in the accounts (the exception, perhaps, is advances).

Attention

Small businesses may not fill out the ODDS at all.

Therefore, many “clean” revenue and other income from VAT by calculation: they take the annual amount of revolutions for the debit of accounts 62, 60, 76 in correspondence with the credit of accounts 51, 50 and other “cash” accounts. And the resulting amount is multiplied by 18/118, thereby highlighting VAT. The remaining amount will be the sum of the proceeds without tax. But this option is suitable only for those who sell goods, work or services taxable only at the rate of 18%. If there are transactions that are taxed at a rate of 10% or are not taxed with VAT, things get complicated. In order to isolate VAT by calculation, you will first have to divide the cash flows from operations taxed at different VAT rates. To do this, some open sub-accounts for settlement accounting accounts.

Similarly, they are “cleared” of VAT and the amount of their own payments.

The resulting difference is shown as cash flows from current operations:

- <если> the difference is positive, it must be taken into account when calculating the indicator on line 4119 “Other income”;

- <если> the difference is negative, it is reflected in parentheses on line 4129 “Other payments” (together with other other payments).

True, often accountants ignore the requirements of the “cash” PBU 23/2011 and do not isolate VAT flows at all. Let's see how the auditors respond to this.

EXPERIENCE EXCHANGE

General Director of the Audit Firm Vector Development

“Regulatory documents do not allow either to choose a way of presenting reporting indicators, or refuse to fulfill the requirement to isolate VAT, because it is“ difficult ”or“ long ”. Therefore, the auditor is forced to indicate such a distortion. However, we do not always include the corresponding reservation in audit report - sometimes limited to a description of the violation in the auditor's report. We believe that not every violation of regulatory requirements makes reporting unreliable, but only such a violation that distorts the user's reporting on real financial condition and the results of the audited entity. If the audited entity in the explanations to the statements indicates that its cash flows are not “cleared” of VAT, the user can still draw the correct conclusions from these statements. ”

As you can see, if it is not possible to allocate VAT flows, you need to inform about this in the explanations - so as not to mislead users of accounting.

Whether to show salary and “salary taxes” together or not depends on your priorities

On line 4122, payments “in connection with the remuneration of employees” must be indicated. It is clear that when filling out it is necessary to take into account salaries, vacation pay, bonuses, and so on. But is it necessary to reflect on it also the amount of "salary taxes" (personal income tax and compulsory insurance contributions)? Here opinions are divided.

APPROACH 1. As payments related to the remuneration of employees, we show on line 4122 the amounts issued / transferred to employees, excluding the movement of personal income tax and insurance premiums. That is, this is the turnover for the year on the debit of account 70 “Settlements with personnel for pay” in correspondence with the credit of accounts 50 “Cashier” and 51 “Settlement accounts”.

And here the paid personal income tax and insurance premiums we show on line 4129 "other payments". However, the same as other taxes (with the exception of income tax).

With this approach you can see where it was the money that went: to employees or to the budget and extra-budgetary funds.

APPROACH 2. On line 4122 we indicate any movement of money that is due to the accrual of "labor" payments. Including the payment of "salary taxes." Then it will be clear how much the organization pays for the "maintenance" of employees. And who exactly is the recipient of money ( budget system or employees), for organizations that use this approach, is not so important.

In order for users of accounting to be clear on what principle your organization is filling out line 4122 of the cash flow statement, it is better to reflect this in the notes to the statements.

Not every movement of money should be reflected in ODDS

Any payments and receipts that do not change the total amount of cash and are not equivalent to cash flows are not sub. “D” p. 6 PBU 23/2011, including:

- transferring money from one bank account to another;

- cash withdrawal from a current account with a bank and, conversely, crediting to the account of proceeds and other cash receipts.

Therefore, such operations do not need to be taken into account when filling out the ODDS.

We show some cash flows minimized, while others - expanded

It all depends on how important these flows are for a particular organization and how they characterize its activities. For example, when filling out the ODDS, the revenue for ordinary activities not reduced by the amount of expenses associated with it.

Cash flows can be minimized, for example, if receipts from one person determine the corresponding payments to other people and / or the flows characterize the activities not so much of the organization as its counterparty to p. 16, 17 PBU 23/2011. In particular, it is possible to show minimized settlements on intermediary agreements, the amounts paid and received upon reimbursement of utility bills under a lease agreement.

Income tax payments should be broken down into three types of operations

To correctly fill in the ODDS, it is necessary to determine which operations were the source of profit from which advance payments and tax were paid (rather than accrued) reporting year at sub. “D” p. 9, p. 7 PBU 23/2011:

- <или> current e p. 9 PBU 23/2011;

- <или> investment p. 10 PBU 23/2011;

- <или> financial p. 11 PBU 23/2011.

Attention

If the classification of flows cannot unambiguously determine their type, they relate to the current operation p. 12 PBU 23/2011.

If the entire income tax transferred to the budget was related to profit from ordinary activities, its amount should be reflected in the current operations on line 4124. For this, in most cases (if, for example, there was no refund of income tax from the budget ) it is enough to take the annual turnover on the debit of the sub-account “Profit tax” of account 68 and the credit of account 51 “Settlement accounts”.

Cash equivalents are also cash

ODDS should include data on the movement of not only money, but also cash equivalents. These are highly liquid financial investments that can be easily converted into a predetermined amount of cash, they are subject to insignificant risk of changes in value and p. 5 PBU 23/2011. For example, it can be open in credit organizations demand deposits, bearer bills of Sberbank Letter of the Ministry of Finance dated 10.15.2012 No. 07-02-06 / 246.

Recall that cash equivalents, together with financial investments, are recorded on the same account 58. However, they are a special type of asset. IN balance sheet they should be shown under the item “Cash” (line 1250), and not under the item “Financial investments” (line 1170). If the organization has cash equivalents, special attention should be paid to the correspondence of the ODDS and balance sheet indicators.

When filling out the report, carefully convert the foreign currency into rubles

When filling in the lines of receipt and disposal of foreign currency / currency equivalents, take the ruble amount of operations from the accounting data as of the date of operation. That is, the conversion rate to rubles is taken on the date of the movement of money (on the date of operation). At these individual rates, currency flows will be taken into account when calculating the indicator for line 4400 “Cash flow balances for reporting period».

- increase financial soundness companies through the rational use of borrowed funds;

- improving the solvency of the company;

- risk reduction (cash gap);

- rational use of cash.

The construction of a cash flow accounting system is a complex process, the automation of which should be preceded by the stage "The construction of an accounting system and the development of cash flow regulations"

This stage can be divided into the following tasks:

- cash flow structuring;

- creation of regulations for the main cash flow management processes

Cash Flow Structuring

Cash flow and its structuring is, in essence, the development of the analytical reference “Turnover Articles”.

The set of analysts and the structure of the directory for cash accounting should ensure the completeness of the analytical sections of planning, which will allow you to see the separation of cash flows by types of cash flows, generate the necessary analytical reports and eliminate the risk of a cash gap.

At the most basic level, the set of cash flow planning articles should be consistent with the cash flow statement analysts.

Cash flow articles, with an example of a structured directory

Cash flows from current operations

- Income:

- from the sale of products, goods, works and services, rental payments, royalties, royalties, commissions and other similar payments;

- from resale of financial investments;

- other supply;

- Payments:

- suppliers (contractors) for raw materials, materials, work, services;

- in connection with the remuneration of employees;

- interest on debt obligations;

- income tax;

- other payments;

- Income:

Cash flows from investing operations

- Income:

- from sale non-current assets (except for financial investments);

- from the sale of shares (participatory interests) in other organizations;

- from repayment of loans granted, from sale of debt valuable papers (rights to claim cash to other persons);

- dividends, interest on debt financial investments and similar proceeds from equity participation in other organizations;

- other supply;

- Payments:

- in connection with the acquisition, creation, modernization, reconstruction and preparation for use of non-current assets;

- in connection with the acquisition of shares (stakes) in other organizations;

- in connection with the acquisition of debt securities (rights to claim cash to other persons), the provision of loans to other persons;

- interest on debt obligations included in the cost of the investment asset;

- other payments;

- Income:

- Cash flows from financial transactions

- Income:

- obtaining loans and borrowings;

- cash deposits of owners (participants);

- from the issue of shares, increase in interests;

- from issuing bonds, bills and other debt securities, etc .;

- other supply;

- Payments:

- owners (participants) in connection with the redemption of their shares (stakes) of the organization or their withdrawal from the participants;

- on the payment of dividends and other payments for the distribution of profits in favor of owners (participants);

- in connection with the repayment (redemption) of bills and other debt securities, repayment of loans and borrowings;

- other payments;

- Income:

The directory is organized in such a way that at the first level of the groupings are “Types of cash flow items”, and in subordinates the cash flow items themselves.

The development of cash management regulations will streamline business processes associated with the use of company funds.

The regulations should include the structure of cash flow planning documents (both strategic and operational), a description of the approval and approval of the DDS plan.

The cash flow structure of the approval of documents may vary depending on the type of planning document (DDS budgets, requests for DS consumption).

In addition to the composition of the documents and the list of persons involved in the coordination, it is necessary to determine the terms of approval, ensure the procedure for entering documents, so that the treasurer has time to manage payments, and ensure that unplanned payments can be registered.

The software product “WA. Financier: Cash Management”, developed on the basis of 1C 8, gives the user a reliable tool for building a cash management system, and also allows you to timely identify the cash gap, establish the causes and take measures to eliminate it.

The reference book “Budget Turnover Articles”, in addition to the hierarchical structure, has a number of details:

- Details used in the formation of reporting forms:

- Name

- The name is not a foreign language

- Reporting Code

- Used by the system and increasing the analytical capabilities of the directory:

- Direction of travel

- Type of cash flow item

- Article Analysts

- Details enhancing administration

- Access group

- Analytics validity period

Using this guide will allow the user to develop a structure of planning articles of any complexity, in accordance with the needs of the business.

Money is the most liquid part of operating assets and represents cash on hand, as well as on settlement, current, currency, deposit and special accounts. The main source of data on their movements is form No. 4 of accounting statements Cash flow statement in 1C, where it is possible to conduct analytical accounting in the context of articles of DDS. Cash flow items in 1C are additional analytics (subconto) for some accounting accounts, for example, accounts 50 / Cashier and 51 / Settlement accounts.

Another source of information about the movement of money is the management report “Cash Flow Analysis”. In order to form a ODDS form or such a report, you must configure the cash flow items in 1C 8 (configure the DDS articles in the "DDS Articles" directory). Its correct maintenance and timely completion of the required articles of the DDS in the relevant documents of the Bank and Cashier section is the key to the correctness of the report.

So, we consider the tools for accounting in the context of DDS in the program 1C Accounting 8.3.

Setting up a chart of accounts

To work with the article directory, you must first make the settings, which are located in the section “Administration / Accounting parameters / Setting up a chart of accounts / Accounting for DDS: By r / s and articles of DDS” or in the section "Main / Chart of accounts / Setting up a chart of accounts."

Figure 1 Setting up accounting for DDS by articles

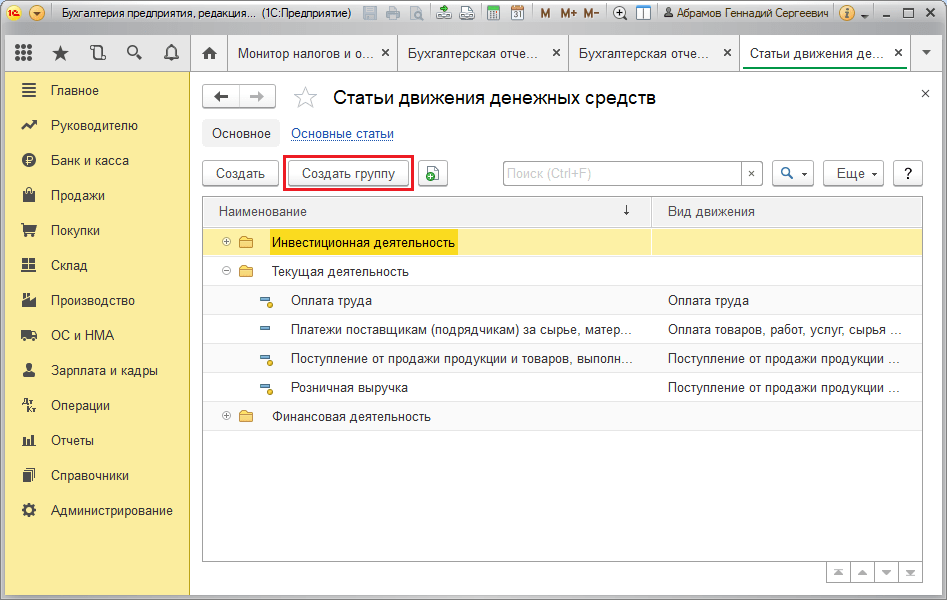

Handbook "Cash Flow Articles"

This directory is located "Directories / Bank and cashier / Articles DDS."

Since the financial flows of the company are classified according to three types of work - daily, related to investment, as well as finance, the DDS articles in the directory can be combined into the appropriate groups. To do this, use the "Create Group" button.

Figure 2 Article Directory

Figure 2 Article Directory

We give examples of types of DDS with classification by type of activity.

Table "Examples of types of DDS"

Consider filling out the details of the article directory element.

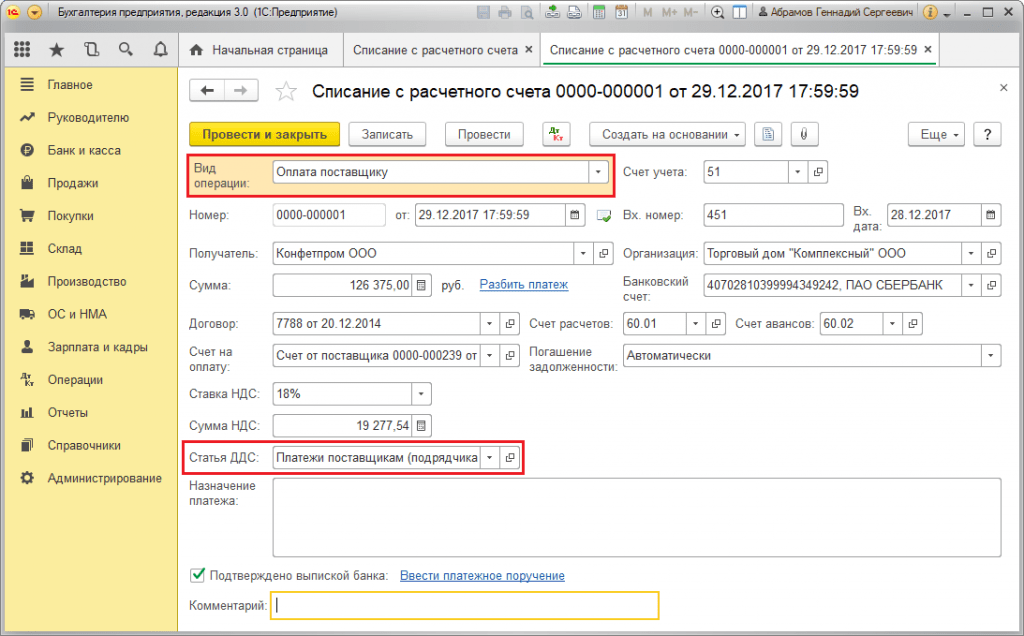

The props “Use by default in operations” correspond to the props “Type of operation” in the documents of 1C Accounting 8.3 program and are used to automatically substitute the DDS article in the corresponding line of the document for receipt or consumption of cash

Figure 3 The “Use by default in operations” attribute of the article directory item

Figure 3 The “Use by default in operations” attribute of the article directory item

Figure 4 Props “Type of transaction” and “Article of DDS” in the document “Write-off from the current account”

Figure 4 Props “Type of transaction” and “Article of DDS” in the document “Write-off from the current account”

The values \u200b\u200bof the “Movement type” attribute correspond to the lines of form No. 4 “DDS Report”. The types of cash flows are predefined, that is, the types of DDS in 1C 8.3 are not intended for editing.

Figure 5 Props "Type of movement" of the element of the directory of articles DDS

Figure 5 Props "Type of movement" of the element of the directory of articles DDS

The DDS articles created in the reference book serve to fill in the requisite “DDS Article” in the program documents. For example, in the bank's documents “Receipt to r / s” and “Write-off from r / s” or cash desk - receipt and expenditure cash warrants.

Form No. 4 “Cash Flow Statement”

The annual accounts for the fourth form can be formed in the section “To the Head / Tax and Reporting Monitor / Accounting Statements”.

Figure 6 Form ODDS

Figure 6 Form ODDS

The amounts of money registered under the articles, when creating the report form, will be attributed to one or another type of DS movement, depending on the articles specified during the relevant documents.

Let us demonstrate the above with an example. Suppose, through “Receipts to the railroad”, under the article of movement “Receipts from the sale of products and goods, performance of work, rendering of services”, payment from the buyer in the amount of 102 135.00 rubles, including VAT of 15 579.92 rubles, was recorded.

Figure 7 Props "Article DDS" of the document "Receipt on the account"

Figure 7 Props "Article DDS" of the document "Receipt on the account"

In the configuration of the article we are considering, the type of movement of the same name is indicated.

Figure 8 Setting up a sales receipt

Figure 8 Setting up a sales receipt

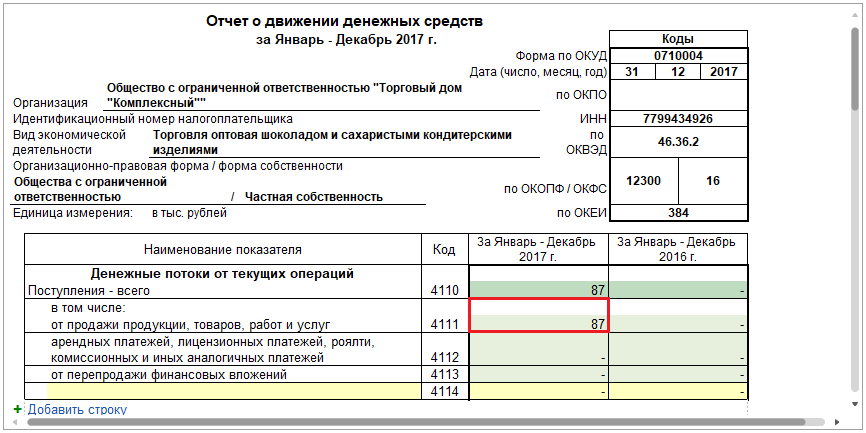

Thus, the registered payment from the buyer under the DDS article with the type of movement “Income from the sale of products and goods, performance of work, rendering of services” on form No. 4 of the report will be included in the total amount on line 4111 “Income from the sale ...”.

Figure 9 Payment from the buyer in ODDS

Figure 9 Payment from the buyer in ODDS

Decoding on line 4111 allows you to see the components of the total amount for this line. In our example, the total amount of 87 thousand rubles was received as the difference between the amount of payment from the buyer 102 135.00 rubles and VAT 15 579.92 rubles (86 555.08 ~ 87 thousand rubles).

Figure 10 Interpretation on line 4111 "Proceeds from the sale ..."

Figure 10 Interpretation on line 4111 "Proceeds from the sale ..."

Cash Flow Analysis Report

This management analytics is available to “Manager / Cash”.

In order for the information in the report to be grouped by DDS, in the report settings, on the "Grouping" tab, select the "Cash flow item" check box. Report settings are hidden under the “Show settings” function button.

Figure 11 “Cash flow analysis” report

Figure 11 “Cash flow analysis” report

Figure 12 Report Settings

Figure 12 Report Settings

Assessment of the status of DDS

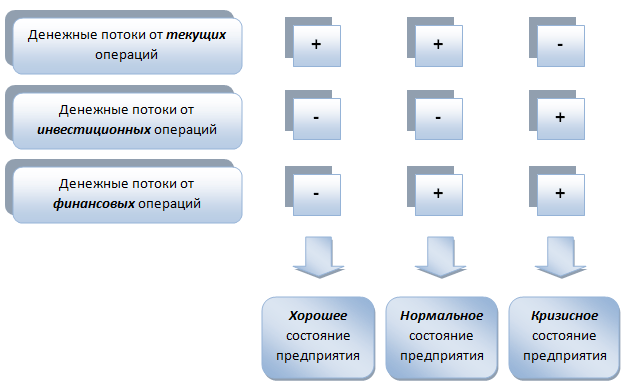

ODDS is an informational basis for the analytical conclusions of cash flows. According to their condition, we can conclude about the level of enterprise management.

Figure 13 Analysis of the quality of enterprise management depending on the structure of cash flows

Figure 13 Analysis of the quality of enterprise management depending on the structure of cash flows

When the mass of the net cash flow from current operations for the reporting period matters in positive territory, and from investment and financial operations, respectively, in negative territory, the state of the company is considered good. When the cash flow as a result of current and financial operations for the reporting period goes to plus, and as a result of investment operations - to minus, they talk about the normal state of affairs of the enterprise.

An enterprise is in crisis if the value of net cash flow from current operations is negative, and from investment and financial transactions - positive. The most correct situation is when the amount of net cash flow for all types of business processes is of positive value.

Comments : In the process of financial and economic activities, organizations carry out settlements with counterparties in cash or non-cash.

The procedure for conducting cash transactions is regulated by a regulation approved by the Central Bank of the Russian Federation, in accordance with which, for their implementation, it is necessary:

the presence of a specially equipped checkout room equipped with a burglar alarm;

maintaining a cash book and other cash documents of the established form;

organizations accept cash at settlements with individuals with the obligatory use of cash registers;

spending cash received from banks strictly for the purposes indicated on the check;

cash storage at the cash desk within the limits established service bank after agreement with the management of the organization.

The exception is the money taken from the bank for payment salarysocial security benefits and scholarships. Funds earmarked for these purposes may be kept at the organization’s cash desk for three business days, including the day the money was received at the bank.

The facts of receipt and expenditure of funds are drawn up according to incoming (FFP) and consumables (CSC) cash orders. Cash flow accounting at the checkout is carried out in Cash registerthe book. To account for the presence and movement of cash at the checkout, the active account 50 "Cashier", subaccount 50.01 "Cashier of the organization" is used. Analytical accounting in a standard configuration is organized using the directory Cash flow items, what is necessary for automatic formation “Statement of cash flows.

To make settlements in non-cash form, organizations can open settlement and current accounts with banks. The current account is the main account of the organization through which all monetary transactions are conducted without limiting their list. Current accounts are opened in cases when there is a separation of any operations. Current accounts include: foreign currency, on transactions with funds for special purposes, due to the peculiarities of settlements, etc.

Receiving and issuing money from a current account or cashless payments are made by the bank on the basis of relevant documents, the most common of which are: cash payment announcement, cash check, payment order, settlement check, payment request.

Upon receipt of cash flows, the organization receives from the bank Statement from settlement, currency and other accounts with attached copies of documents on the basis of which funds were credited or debited.

To account for transactions in the current account, the active account 51 “Current account” is intended. Analytical accounting in a standard configuration is organized using directories Cash Flow Articles and Bank accounts

.16

Fill In The Handbook Cash Flow Articles

|

Name |

Type of cash flow (DDS) |

|

Income from the founders |

Other income for investment activities |

|

Equipment purchase |

Acquisition of fixed assets |

|

Payment for installation work |

Other investment expenses |

|

Procurement of materials |

Payment for goods, work, services, raw materials and other current assets |

|

Tax transfer |

Payments for taxes and fees |

|

Disbursement of funds under the report |

|

|

Other cash inflows |

Other income from current activities |

|

Other cash expenses |

Other current expenses |

|

Cash withdrawal at the bank |

|

|

Handing over cash to the bank |

Command - Cashier - Cash Flow Articles - Action - Add

In props Name- Income from the founders

In props Cash flow itemby clicking on the button open the list and select - Other income from investment activity - Enter

Similarly, enter in the directory articles cash flow absent in the infobase.

.17

Write out 01/16 of this year Incoming cash warrants to founders - to individuals in accordance with the constituent agreement of 08.01 of this year, according to which, each founder of ELF LLC must deposit 50% of its share in cash to the cash desk or to the account of the company.

|

Founders |

Amount (rub.) |

Document |

|

Antonov S.V. |

30000 |

PKO No. 1 |

|

Semenova O.P. |

12500 |

PKO No. 2 |

|

Gruzdev V.A. |

15000 |

PKO No. 3 |

|

TOTAL |

57500 |

Command -

Other parish - OK

Room -default, Date -January 16, 2011 - Organization -LLC "ELF", accounting account -50.01, Amount -30000.

On the bookmark Payment Details - Account -75.01, Counterparties -Antonov S.V., Cash flow item -Income from the founders

On the bookmark Print - Accepted from- Antonova S.V. - Base -Memorandum of Association of January 8, 2011 - Application -Extract from the memorandum of association of ELF LLC - Write down

Print - Close - OK

Similarly, enter information on the remaining founders.

.18

Write out a consumable cash warrant from January 16, 2011 for delivery by the cashier Viktorova S.S. cash from the cash desk of the enterprise in the amount of 57,500 rubles. to the current account of the company in the JSCB DONKOMBANK.

Command - Cashier - Account cash warrant - Actions - Add

Selection of the type of document operation -Cash deposit to the bank - OK

Room -default, Date -January 16, 2011 - Organization -LLC "ELF", accounting account -50.01, Amount -57500.

On the bookmark - Score -51, DDS Article -Handing over cash to the bank

On the bookmark Print - Issue- Victor Svetlana Sergeevna. - Base -Delivery of contributions of founders from the cash desk for crediting to the current account - Write down

View the printed form of the document - Print - Close - OK

Comments : Operations on the movement of cash to the current account from the cash desk and back, at the same time refers to banking and cash operations. The fact of these operations is confirmed as cash ( RKO, PKO) and bank documents ( Statement) Each document generates an entry in the Operations Log, but postings are only generated based on cash register document, in order to avoid duplication of reflection of the same operation on accounts accounting.

.19

To create a cash book for January 16, 2011

Command - Cashier - Cash Book -16.01 - To form

Check Digit: 0 - Balance at the end of the day

.20

Generate a bank statement dated January 16, 2011 using bank statement processing.

16.01.T. Bank statement No. 1 was received on transferring 57500 rubles to the account of the enterprise.

|

AKB DONKOMBANK Processing date 1/16/2011 Account 40702810944230000123 Incoming balance Passive 00.00 |

||||||

|

date |

№ dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

16.01 |

57500.00 |

|||||

|

Outgoing balance Liabilities 57500.00 |

||||||

Note:The amount of receipt is reflected in the column. Credit(as for a bank, crediting funds to a current account is an increase accounts payable in front of the client) , and consumption - in the column Debit(reduction of debt to the client).

Command - Bank - Bank statement -January 16, 2011

Since this statement is based on RKO No. 1, the statement will contain a record dated January 16, 2011. in the amount of 57,500 rubles.

Check Digit: 57500 (SK Dt sc. 51 Reports - WWS according to sc. 51)

.21

Register payment orders incoming from 19.01. this year

Generate a bank statement dated January 19, 2011

According to the memorandum of association, each founder of ELF LLC must contribute at least 50% of his share in the authorized capital in the form of a cash contribution. In accordance with this agreement, 01/19 TG to the current account of ELF LLC funds were credited as deposits in the authorized capital of LLC SIGMA 50,000 rubles. (payment order No. 23) and OJSC ECOS 42500 rubles. (payment order No. 98). 01/19 TG Bank statement No. 2 was received confirming the receipt of funds from the founders.

|

AKB DONKOMBANK Processing date 01/19/2011 Account 40702810944230000123 Personal account of ELF LLC TIN 6164186537 Incoming balance Passive 57500.00 |

||||||

|

date |

№ dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

19.01 |

50000.00 |

|||||

|

19.01 |

42500.00 |

|||||

|

Outgoing balance Liabilities 150,000.00 |

||||||

Command - Bank - Bank statements - Actions - Add

Selection of the type of document -Receipt to the current account.

Selection of the type of document operation -Other income

Reg. number -default, from -01/19 TG, accounting account -51, in. number -23, from -01/19 TG, Payer -SIGMA LLC, C payer's even -choose, amount -50000.

Score - 75.01, counterparties -SIGMA LLC

DDS Article - Income from the founders - OK.

Similarly, enter payment order incoming No. 98

Check Digit: 150000 (SK Dt sc. 51 Reports - Card count. 51)

.22

Write out a cash receipt order No. 4 of 01/20 of this year Generate a bank statement dated January 20, 2011

The director of ELF LLC gave an oral order to the cashier to receive 3,500 rubles from the current account. cash for current household expenses. January 20, 2011 from the current account of ELF LLC to JSCB DONKOMBANK under check Р07 No. 467875 dated January 20, 2011 received funds for household expenses - 3500 rubles. January 20, 2011 Bank statement No. 3 was received, confirming the fact of this operation.

|

AKB DONKOMBANK Processing date 01/20/2011 Account 40702810944230000123 Personal account of LLC Elf TIN 6164186537 Incoming balance Passive 150000.00 |

||||||

|

date |

№ dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

20.01 |

3500.00 |

|||||

|

Outgoing balance Liabilities 146500.00 |

||||||

Command - Cashier - Incoming Cash Order - Actions - Add

Selection of the type of document operation -Cash withdrawal at the bank - OK.

Room -default, Date -January 20, 2011 - Organization -LLC "ELF", accounting account -50.01, Amount -3500.

On the bookmark Payment Details - Bank Account -Settlement in JSC AKB DONKOMBANK - Credit score -51, DDS Article -Cash withdrawal at the bank

On the bookmark Print - Accepted from- Viktorova Svetlana Sergeevna - Base -Received under check Р07 No. 467875 for household expenses - To record.View the printed form of the document - Print - Close - OK.

Check for a statement of discharge dated January 20, 2011 In the magazine Bank statements

Check Digit: 146500 (SK Dt sc. 51 Reports - WWS according to count 51)

.23

Analyze cash flow for January using the reporting forms Subconto Analysis and Account Analysis 50.01 (51)

Command - Reports - Subconto Analysis Types of Subconto - Cash flow items - Generate a report.

The sub-analysis analysis report shows that each type of cash flow does not have a balance at the end of the reporting period. Total end debit balance in the reporting form, the analysis of the account -150000 (SK Dt) shows the balance of cash accounts as of January 20, 2011 (Account card 51). Including SK Dt. 50.01 - 3500, SK Dt. 51 - 146500.

Command - Reports - Analysis of account 51 (50.01)

2.2.3 Accounting for settlements with contractors for core activities

Comments: Currently, settlements with customers are carried out both in the preliminary order and in the order of subsequent payment. Cash received as a prepayment to the current account of the enterprise is recorded as payables to the buyer finished products. The reason for entering into information base prepayment is a Bank statement confirming the receipt of funds to the current account.

In case of prepayment (advance payment), the company that received it must pay VAT to the budget, which is included in the amount of prepayment, because prepayments and down payments are included in tax base VAT included. Therefore, upon receipt of cash as a prepayment (advance) on the basis of Bank statement in Posting Journal two entries are made:

Dt 51 “Settlement accounts” - Kt 62.02 “Advances received” - in the amount of the prepayment (advance) actually received

Dt 76.AV “VAT on advance payments and prepayments” - Kt 68.02 “Value Added Tax” - for the amount of VAT contained in the amount of the received prepayment (advance). The basis for this wiring except B subscriptions the jar serves Invoice issued, which is formed by the supplier upon receipt of funds associated with the calculations for the payment of goods (work, services).

Invoicedrawn up upon receipt of prepayment, is the basis for settlements on value added tax.

Buyer registration in the directory Counterparties;

Document Registration ( Of the agreement), which is the basis for the receipt of funds;

Enter Incoming Payment Orderconfirmed Bank statement

Statement and registration of invoice for advance document Invoice issued.

In the event that settlements are made after the actual shipment of products to customers, the basis for completing settlement relationships for a particular transaction is Bank statement, according to which the repayment is recorded accounts receivable the buyer (Dt 51 "Settlement accounts" Kt 62.01 "Settlements with buyers and customers").

Settlements with suppliers are usually carried out in non-cash form by issuing payment orders, which, in turn, are issued on the basis of suppliers' accounts. No postings are made based on the payment order. Reason for accounting entries on a paid order serves Bank statement for the indicated amount, the appendix of which is this payment order.

Payment and final payment for goods received is reflected by posting Dt 60.01 “Settlements with suppliers and contractors” - Kt 51 “Settlement accounts”;

Prepayment (advance payment) for future deliveries - Dt 60.02 “Settlements on advance payments issued” - Kt 51 “Settlement accounts”

The accounting procedure algorithm is implemented in a typical configuration as follows:

Supplier registration in the directory Counterparties

check in Payment order outgoingusing a document Payment orderor processing Bank statement (type of operation Write-off from the current account)

.24

To register in the Counterparties Directory a supply contract concluded with SIGMA LLC

Enter the payment order incoming from 01.21 tg. in the amount of the advance received from the buyer of SIGMA LLC

In accordance with the agreement № ДП \\ 1 from 15.01 of this year an advance payment from SIGMA LLC has been received to the bank account of ELF LLC on account of the upcoming delivery of furniture. This fact in the amount of 300,000 rubles. (including 18% VAT) is confirmed by extract No. 4 of January 21, 2011 with the application of payment order No. 44 of January 21, 2011

Command - Enterprise - Counterparties - Legal entities - SIGMA LLC

On the bookmark - Accounts and contractsin the tabular part Counterparty Agreementsopen form main contract

In field Namechange the default value to - Contract No. DP / 1 dated January 15, 2011

In field Price Type -The main selling price is OK.

|

AKB DONKOMBANK Processing date 01/21/2011 Account 40702810944230000123 Incoming balance Passive 146500.00 |

||||||

|

date |

dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

21.01 |

300000.00 |

|||||

|

Outgoing Balance Passive 446500.00 |

||||||

Command - Bank - Bank statements - Add,document type selection - Receipt to the current account,selection of the type of document operation Payment from the buyer -enter the details of payment order No. 44 of January 21, 2011

Check for a record of Statementfrom January 21, 2011 In the magazine Bank statements

Check postings recorded in accounting based on Statementsfrom 21.01.t.g. , Command - Bank - Bank settlement documents -move the cursor to the line with the corresponding entry - click the icon.

.25

Generate an invoice issued in advance on January 21, 2011

Register an invoice for advance payment from 01.21 tg. in the Sales Book.

Command - Sales - Maintaining sales books - Registration of advance invoices -indicate the period for which it is necessary to generate invoices for advance payment - Fill - Run

Command - Sales - Maintaining sales books - Creating sales book entries - Actions - Add. Room -default, from -January 21, 2011, on the tab - C Advances - Fill

Check digit : 45762.71 - amount of VAT

.26

Check the registration of the invoice dated January 21, 2011 in the Sales Book.

Command - Sale - Keeping a sales book - Sales book - January - Form

.27

Register the counterparty FGUP PLANT No. 324 in the Counterparties directory

ELF LLC has concluded with FSUE PLANT No. 324 agreement No. DP / 3 dated January 17, 2011 on the supply and payment of equipment “Format-cutting machine SFR-2” in the amount of 1 pc. in the amount of 180,000 rubles., including VAT 18%.

|

Information about the counterparty FGUP ZAVOD No. 324 |

|

|

Full name |

Federal State Unitary Enterprise PLANT No. 324 |

|

Brief |

FSUE PLANT № 324 |

|

Legal address |

344081, Rostov n / a, st. Machine Tool Builders, 9. |

|

INN / KPP |

6164345656/616400002 |

|

OKPO |

58493671 |

|

Checking account |

40702810400000000217 |

|

In the bank |

OJSC AKB Selmashbank, 344018, Rostov n / a, 76 Semashko |

|

Corr. Score |

30108104000000000860 |

|

BIC |

046015860 |

Command - Purchase - Counterparties - Legal Entities - Actions - Add -Fill in the form with the relevant details on the bookmarks General, Addresses and Phones, Accounts and Agreements.

On the bookmark Accounts and contractsenter information on the counterparty’s bank account and equipment supply agreement in the field Type of contract - With the supplier.

.28

Register a Payment order outgoing from 01/23 of this year for advance payment of production equipment in one of two ways.

January 23, 2011 an extract was received, accompanied by payment order No. 1 dated 23.01, which stated that the amount of 180,000 rubles. transferred to the account of the supplier FSUE PLANT No. 324

|

AKB DONKOMBANK Processing date 01/23/2011 Account 40702810944230000123 Personal account of LLC ELF TIN 6164186537 Incoming balance Passive 446500.00 |

||||||

|

date |

dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

23.01 |

180000.00 |

|||||

|

Outgoing balance Liabilities 266500.00 |

||||||

Command - Bank - Payment order - Actions - Add - sfill in the necessary details - DDS Article -Acquisition of fixed assets - Record - View the printed form of the document and check the availability of the corresponding entry in Bank statement for 23.01. this year

This document can also be generated using processing. Bank statement (type of operation Write-off from the current account).

Check Digit: 27457.63 - the amount of VAT in the payment order.

.29

Generate payment order No. 2 of January 25, 2011 for advance payment to the supplier of OJSC "ECOS" for materials in the amount of 48331.62 rubles. under the contract No. ПМ 15/2 dated January 18, 2011 and check the relevant Bank Statement.

Generate payment order No. 3 dated January 27 for advance payment of ECOS OJSC for materials in the amount of RUB 35,803.56. under the contract No. ПМ 17/3 dated 10.02 of this year and check the relevant Bank Statement.

|

AKB DONKOMBANK Processing date 1/25/2011 Account 40702810944230000123 Personal account of LLC ELF TIN 6164186537 Incoming balance Liabilities 266500 |

||||||

|

date |

dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

25.01 |

48331.62 |

|||||

|

Outgoing balance Liabilities 218168.38 |

||||||

|

AKB DONKOMBANK Processing date 1/27/2011 Account 40702810944230000123 Personal account of LLC ELF TIN 6164186537 Incoming balance Passive 218168.38 |

||||||

|

date |

№ dock |

BIC |

Correspondent number accounts |

Debit |

Credit |

|

|

27.01 |

35803.56 |

|||||

|

Outgoing Balance Liability 182364.82 |

||||||

.30

Check the status of accounts payable for settlements with suppliers for January and the balance of the current account on January 27, 2011

Command - Reports - Balance sheet for the account. 60.02 - 01.01 - 27.01 - Form

Command - Reports - Account card - 01.01 - 01.01 - count. 51 - Form

Check digits: 264135.18 (SK Dt according to the account 60.02); 182364.82; (SK Dt. Count 51)

Real estate investment

Available online deposits in VTB

To whom and on what conditions they give a mortgage in a savings bank

Rosbank entrance for legal entities

What to specify for credit purposes