The flip side of increased sales is almost always an increase in accounts receivable. In the modern post-crisis situation, increasing production and sales is no longer key factor company development. The main indicator of stability is competent control, planning and management of receivables.

At the stage of making a decision to provide a loan to a buyer, the following are of primary importance:

- the validity period of the contract for deferred payment (as a rule, standard contracts with a predetermined loan period are used);

- the level of solvency and reliability of the client, while special attention when collecting information is paid not only to open sources, but also to unofficial ones (for example, personal connections in regulatory and law enforcement agencies);

- creation of a system of reserves in case of occurrence bad debt. The most reliable and honest client, on the basis of any standard contract, is exempt from liability in the event of force majeure circumstances, and although force majeure circumstances are rarely the real reason for non-payments, they should not be discounted;

- creation of a reliable mechanism for working with problem payers. As a rule, this responsibility is assigned to the enterprise security service. In addition, financial instruments are used, such as charging a penalty for each day of delay, including the day of payment, revising the terms of the contract as a whole;

- providing a discount, the size of which is inversely proportional to the loan term. Thus, the client becomes interested in repaying the debt as quickly as possible.

First, the level and dynamics of debt in the previous period are analyzed using the formula:

Kdz = Z/A,

where Kdz is a coefficient showing the level of involvement working capital in accounts receivable;

Z - amount of debt;

A is the total amount of working capital.

An important indicator of the quality of receivables is the turnover rate of working capital invested in debt, which is calculated using the following formula:

KO = OR/Z,

where KO is the number of rotations of the remote control in the period under review;

OR - the amount of turnover in the period under review;

After this, the level of bad debt is determined using the formula:

Kpr = Zpr/Z,

where Kpr is a coefficient expressing the level of overdue debt;

ZPR - debt not paid under the contract in the period under review;

Z - the amount of debt in the period under review.

Then the efficiency ratio of investing working capital in accounts receivable is determined:

Edz = Pdz - Zdz - Pdz,

where Edz is the efficiency ratio of invested funds in receivables;

Pdz - profit received due to sales on contractual terms;

Zdz - costs associated with lending (verification, work with debtors, etc.);

Pdz - the amount of financial losses from non-repayment of debts.

Sdz = Or + Ks x (Pdn + Ppr),

where Sdz is the amount of funds invested in accounts receivable;

Or - planned sales volume on credit;

Kc - the ratio of cost and product price;

Pdn is the weighted average of the number of days for which goods are shipped on credit;

Pdr - period of late payments, days.

When a company cannot invest necessary funds into accounts receivable, it is necessary to make an adjustment to the planned revenue and profit received from sales on debt.

One of the new methods of debt management is the refinancing of receivables, the main forms of which are factoring, forfaiting, and bill accounting.

Of particular interest to the company is factoring as a tool that covers a significant amount of supplier risks. In addition, the capital turnover period increases; for a relatively small percentage, the company optimizes the financial structure and does not bear additional expenses on working with problem customers.

One of the key conditions for granting a loan is determining the duration of the agreement. Due to an increase in the duration of the contract, sales volume and revenue increase, but the amount of funds that need to be invested in receivables increases and increases financial cycle companies. Setting a limit loan agreement, it is necessary to take into account all the stated points.

Determining for yourself the importance of each factor, weighing everything potential risks, the company is building its credit policy, which determines credit limit for each individual period.

In combination with the period for which the loan is provided, its cost is of particular importance. Determined by a system of price discounts for immediate payments for the supply of products. Based on these indicators, the interest rate for the loan provided is calculated:

Pg = Cs x 360/Sp,

where Pg is the interest rate on the loan provided;

Tss - discount for immediate payment without deferment;

SP - validity period of the loan agreement.

The peculiarity of establishing this norm is its connection to interest rate By bank loan. In any situation it should be lower than in financial institutions. Otherwise, it is more profitable for the counterparty to take out a loan from a bank and pay for the delivery on an advance payment basis.

Based on the experience of domestic companies, it is possible to create an algorithm showing the degree of responsibility of each employee in the process of managing accounts receivable. As a rule, the commercial division of the company (sales department) oversees sales and receipts. cash, financial service Responsible for information and analytical work. Legal service is responsible for the impeccable state of document flow for problematic shipments ( necessary condition in case of litigation). If the debt becomes problematic, the company’s security service gets involved.

In addition, it is important that the functions of performers when working with a client are not duplicated. Otherwise, there is inconsistency between departments, leading to a decrease in operational efficiency. Therefore, it is necessary not only to clearly distribute functions between departments, but also to clearly describe their actions at all stages of working with a problem client (see table).

Distribution of functions of performers when working with clients

Accounts receivable management stage | Actions of departments for managing receivables | Responsible department |

| Establishing a payment period within the scope of the contract | Signing the contract | Financial Director |

| Issuing an invoice for payment | Sales department | |

| Shipment of goods and support of shipment (issuing invoices, receiving confirmation from the client that the goods have been received in the proper quantity and quality) | Sales department | |

| Reminder of the payment date (three working days before the end of the contract) | Sales department | |

| Control of overdue payments up to 7 working days | Finding out the reasons for the delay in payment | Sales department |

| Coordination of a repayment schedule for overdue debts | Finance department | |

| Stopping further shipments | Commercial Director | |

| Written notification of the commencement of application of penalties | Financial Director | |

| from 7 to 30 working days | Calculation of a fine | Financial Director |

| Daily calls reminding you to pay | Sales department | |

| Personal meeting with the director or owner of the debtor company | Commercial Director, Sales Department | |

| Written notice of preparation for trial | Legal service | |

| from 30 to 60 working days | Repeated personal meeting with the manager or owner of the debtor’s company, taking all possible measures to find a compromise solution | Head of Security Service, Sales Department |

| Official complaint (written) | Legal service | |

| more than 60 working days | Filing a claim in court | Legal service |

An additional incentive that can reduce the number of bad debts is such an unpopular measure as establishing a relationship between bonus payments to sales employees and the state of the company's total accounts receivable. Despite the fact that all divisions of the company, without exception, take part in the process of assessing the solvency of a potential client, his reliability, it is the sales department specialists who are the first link in the chain of starting contractual relations, they always have more reliable and timely information about the state of the market, the solvency of certain counterparties. It is on the basis of information transmitted by the sales department to other divisions of the company that decisions are made to sign or not to sign contracts for deferred payment.

No less responsible is the financial department of the company, whose responsibilities include conducting an error-free analysis of the state of total accounts receivable for the company as a whole. System errors that can be made in this case are no less dangerous for the company’s activities than the occurrence of bad debts due to the collection of incorrect information about potential clients.

Accounting and timely analysis of the status of receivables is currently impossible without the use of special computer programs and accounting automation cash receipts. This is due to an increase in shipment volumes, the number of invoices issued and deferred payment agreements. At the same time, it is possible to perform an analysis not only by counterparties and periods, but also to identify for which product groups and in which price segment bad and problem debts most often arise. This, in turn, allows you to more accurately assess risks when deciding whether to sign an agreement with a particular buyer.

In conclusion, we add that in the process of managing receivables great value have professionalism and a high degree of motivation of the personnel involved in this process. Registration of all necessary documents, confirming the fact of shipment, the imposition of obligations on the counterparty must be fulfilled exactly in established deadlines and in an appropriate manner. Practice knows many examples when the debtor was released from payments during the trial due to the fact that the plaintiff did not submit all the necessary, correctly executed documents confirming the fact of shipment and the provision of a loan.

Accounts receivable are classified:

- by maturity (short-term - payments are expected within 12 months after the reporting date; long-term - payments are expected more than 12 months after the reporting date);

- according to the degree of possibility of collection (current - debt within the payment terms established by the contract; doubtful - the repayment period has already been violated, but the company is confident that the funds will be received; bad - debts that are unrealistic for collection).

Depending on the size of their operations, companies may establish their own classifications of accounts receivable.

How to prevent doubtful and bad debts

There are several ways to prevent or minimize bad debt.

1. Prepayment

If there is a risk of problems with the buyer, it is better to conclude an agreement with him on an advance payment basis. Moreover, the prepayment in this case must be 100%. Then you, as a supplier, will not have problems with debts.

2. Security in the form of collateral, surety, bank guarantee

3. Counter debt (accounts payable)

When there is a counter-debt, you can relatively safely ship products without prepayment, without collateral or other safety net options. If there is an accounts payable and there is accounts receivable, it is always possible to cover them by offset.

4. Letter of credit

This is a rather exotic option, although undeservedly forgotten. A letter of credit is one of the forms of non-cash payments, the meaning of which is as follows: when both parties to a contract (for example, for supply) do not trust each other (that is, the supplier does not trust the buyer, because he is afraid that he will not pay, and the buyer is afraid make an advance payment because you are not sure that the supplier will ship the goods), the problem can be solved by a third independent party represented by a bank (issuing bank).

In this case, the bank opens a letter of credit: part of the funds in the buyer’s current account is transferred to a special account in this bank, and the buyer has no right to dispose of this money for a certain period. The bank then informs the supplier that the money is “reserved” for him in a separate account and this money will be transferred to him as soon as he submits documents confirming the shipment.

Unfortunately, this service is not very popular. Probably because it's not cheap. But from a financial and civil legal point of view, this is a good option for preventing the accumulation of debts.

6 methods of internal control of accounts receivable

It must be said right away that there are no universal methods for controlling accounts receivable. Everything is very specific, and a lot depends on the activities of the enterprise, its scale, the amounts processed, clients, and the market in which the enterprise operates. There are too many factors to consider. However, you can focus on several important criteria.

1. Planned level of accounts receivable

The maximum allowable amount of accounts receivable is determined by calculation. It is expressed in absolute values and/or as a percentage of revenue.

We are talking about the amount of debt that a company can afford without serious damage to its financial and economic activities. It is better to set this amount in a fixed amount, that is, in rubles. Additionally, you can set it as a percentage of revenue.

2. Conditions for providing deferred payment (credit) to clients

The company may have a specific deadline - 15 or 30 days, for example. But one deadline doesn't work for everyone she works with.

If we are talking about a key or regular client, then the period for him may be longer. After all, he, as a rule, makes large orders and regularly fulfills his obligations.

If a new client appears that the company is not yet sure of, then it makes sense to revise the deadline downwards. A problem client needs to set either a minimum period or even insist on prepayment.

3. Employee motivation

It is desirable to develop a system in which wages employee will depend on the maturity of the receivables.

4. Procedure for granting deferred payment to clients

The information collected about him plays a major role in deciding whether to grant a loan to a client.

You can start by analyzing information from open sources and the information that is requested from buyers. How long have they been on the market? Which of their counterparties can you contact for feedback? How accurately are they calculated? A lot of valuable information for analysis can be extracted from the company’s website.

It is best to visit the buyer's office in person. This will give you an idea of how risky it will be to work with him.

5. Determination of parameters for assessing information provided by the client

IN in this case it is important to take into account the availability of property through which it is possible to repay the debt, the size and dynamics accounts payable, potential financial difficulties and solvency problems.

6. Distribution of responsibility for managing accounts receivable between commercial, financial and legal services

It all depends on the scale of the enterprise, but even in a small enterprise it makes sense to determine who is responsible for what in dealing with accounts receivable, and how responsibility is distributed.

From a logical point of view, the commercial department should be responsible for providing deferred payment and exercise control over current accounts receivable. The area of work of the legal department is doubtful and hopeless accounts receivable (personal meetings, negotiations, correspondence, claims, statement of claim). Accounting includes accounting, control over registration and write-off of receivables.

An indicator for tracking all credit funds received into an enterprise's account, allowing one to evaluate the ratio of the company's total financial assets to its debt to creditors.

Using the Debt Ratio

In general, the debt ratio is most often used by the following entities and individuals:

- organizations closely related to foreign economic activity;

- investors studying a specific thematic project and needing data that allows them to determine its future financial prospects;

- management legal entity involved in frequent determination of the effectiveness of management decisions in the reporting period;

- lenders making decisions about issuing loans to a specific sample of clients.

Debt ratio calculation

The procedure for qualitatively calculating the debt ratio involves the use of data obtained from analysis financial statements subject entrepreneurial activity(SPD). The resulting indicator allows you to determine the degree of efficiency of the enterprise in a certain period. In addition, experts are given the opportunity to compare the activities of a specific company and one legal entity or individual entrepreneur with average market indicators.

The following formula is used to calculate the debt ratio:

- CD - debt ratio;

- SZ - total debt;

- SA - total assets.

Decoding the debt ratio

After determining the debt ratio, it is deciphered. In this case, two significant facts should be taken into account:

- If financial assets companies are distributed rationally, then the coefficient does not go beyond the range of 0-1;

- the ideal option for investors and lenders is zero result.

If the company, considering as a kind of quality financial instrument, has a good reputation and confidently holds a position in the market for goods and services, its debt obligations are covered by its own monetary assets.

A debt ratio approaching 1 indicates that SPD is highly dependent on counterparties. The constant shortage of production working capital forces the company to regularly turn to lenders for help, issuing loans at a substantial interest rate.

If during the calculation process the debt ratio exceeds 1, then SPD will lose its chances of becoming a contender for investment from investors and creditors. This indicator is also conclusive evidence that the company is insolvent and does not have the financial resources necessary to repay its loan obligations.

Pay attention! Those SPDs that engage in irrational spending credit funds, may go bankrupt. If their creditors find out that the debt ratio of the borrowing enterprise exceeds 1, then, most likely, the debtor is waiting trial, the results of which may lead to the company simply being declared bankrupt.

The article was written for directors and heads of sales departments who do not yet automatically work with customer debts. Designed to help them quickly implement a template process into their activities

What is it

and why work with it

Everyone who works in b2b has an idea of accounts receivable ( we'll call her "DZ"). This is what you often unreasonably record in your free assets - debts to you from your counterparties. DZ is a normal and understandable phenomenon, you have shipped - the client pays in 5 days. For these 5 days (for example, you have a 5-day payment period specified in the contract), the debt is registered with him. What happens if the client does not pay after 5 days? The letter "P" - it is added to "DZ" and the result is "overdue receivables (OPR)". Why work with her, because the client will pay anyway? If you are ready to wait a year or three until a not very conscientious client pays for the delivery, then you can skip the article.

Popular processes regarding counterparty debts usually include:

- Return of PDZ. To return what we are already owed

- Shipment with remote control. In order not to aggravate your situation if the client does not pay anyway.

Today we will talk about the return of PDZ. This is directly the process from the “TOP 3” customer requests for automation.

Lifehack:

Almost everyone has debt, but systematically Only a few are fighting it. By and large, it doesn’t matter how your company works with it - through business processes or through an xls table. Any consistency will give results. Business processes are cooler in that they will do 65% of someone’s work:

- Launch themselves when debt arises

- Generate letters to the client

- Send tasks to managers

- Control payment deadlines, etc.

Prerequisites

to implement the process in the life of the company

1. Agreements concluded with your clients must contain the following clauses:

- by payment terms (if this is pre- and post-payment, then an indication of their shares)

- penalties and fines in case of late payment

Not specified in the contract? Not best option, but Article 314 of the Civil Code of the Russian Federation will help, according to which payment must occur within a “reasonable time” or within 7 days from the moment of demand upon fulfillment of obligations.

2. Tasks on it should arise spontaneously and systematically. No system = no control = extra burden of kicks, reminders and excuses.

3. There is such an unpleasant “child’s illness in a toy store” - when you want to have both this and that, and also this. You should start with a simple business process, with a minimum of events. There will be a desire to attach a ton of notifications here, agreements on deadlines from the manager to the manager... No need. It’s better if it’s simpler, but it will work right away, and you’ll have time to finish the bows later. Let employees get used to the new work format.

4. There must be responsibility among those executing the process. Those. if the manager receives his percentage regardless of the client’s payment, then he will not be interested in working with the PD.

What does the process consist of?

and what events are included in it

The operating diagram is shown in the figure above. If you work through business processes, then you need to start the events of the scheme the day before the scheduled payment under the contract (if there is no money from the client yet). All options for working with debt are similar in that, depending on the term of the debt, a certain contractor must carry out certain activities to interact with the client regarding this debt. We tried to combine the experience of different implementations and show some average template that can be easily changed to suit your needs.

There are roughly 4 types of activities in the process:

1. The client has a debt, but it is not overdue.

Operating:

- client manager

Documents used:

- payment reminder letter

In this case, our system should already turn on and try to anticipate the occurrence of a delay. The system itself sends a letter to the client reminding that there is no payment from him. Additionally, a task is created for the manager to phone call client.

2. The client has a debt, payment under the contract is 1 day overdue.

Operating:

- client manager

Documents:

- letter requesting to fulfill obligations under the contract

- event in crm about a call to a client and the result of communication

- optional - blocking shipments to the counterparty

The system recorded the moment of overdue payment and automatically reminded the client and manager about this event. The manager must check with the client about the date of payment; if it is within 7 days, then we consider that the entire process is going “as intended.” The manager sets a new payment date, and the system waits for the payment to be processed. It is advisable to obtain a letter of guarantee from the client.

If the manager understands that there is a risk, or the client says that he will pay later than 7 days, then the process is escalated to the head of the sales department (ROP)

3. Payment under the contract is overdue by 2 days

Operating:

- Head of Sales Department (ROP)

Documents:

- letter of pre-trial demand to fulfill obligations under the contract

- event in crm about a call to a client and the result of communication

The ROP connects to the process and communicates with the client. Either he makes an appointment, or in a telephone conversation he clarifies the reasons with the client, sets a new payment date in the system (the measures in each case are varied and depend on the company’s policy). If the payment date exceeds permissible period, escalates the process further.

4. Payment is overdue by 10 days or more.

Operating:

- legal department / security service

All reasonable deadlines for debt have been exceeded - the service responsible for conflict relations is connected. This is usually either a lawyer or security. Their work depends on company policy. Usually, statuses are entered that allow you to track at what stage the task is at (a claim has been filed, penalties have been calculated, etc.)

Total

how to use it

- Download the diagram and process regulations

- We customize “events” to suit your needs

- We edit regulations, write official orders, and launch

- Want to automate? Write to us, we will set up such a process

We automate such business processes on our new edition" ". In it you can customize such a template, put it into operation and adjust it to your realities - add alerts, include new services in the process, add performance indicators for managers, etc. " " are built into the database, so the work will take place in a single interface. Are you interested in this case? Write to us, we will be glad to cooperate!

Good processes!

In accounts receivable analysis, some tasks that at first glance seem complex often turn out to be simple. You just need to understand their essence and use Excel to solve them. Let's learn to identify from the general list those clients whose debt amount is greater than legal costs.

Calculation of the number of overdue days

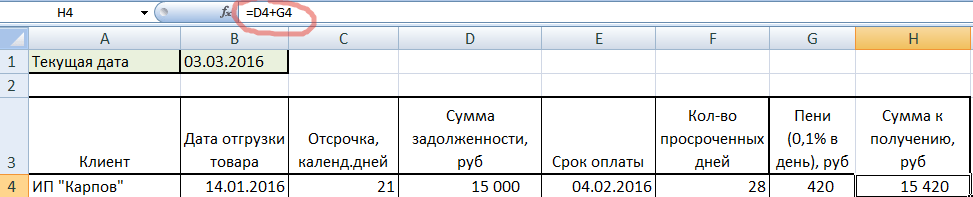

A situation where it is necessary to identify customers with debt may arise in an enterprise that works with deferred payments. That is, for example, the goods are shipped on the 1st, and the buyer is given a delay of 2 weeks. Those. he must make the payment by the 15th. Let's create a basic accounts receivable report in Excel to understand the principle.

In cell B2, the current date is written not in numbers, but in a formula, so that when opening a document, the current date is always entered. The column with the dates of shipment of goods is presented in the DATE format, and with the amounts of debt - in the financial format.

To calculate the number of days overdue on accounts receivable, you need to subtract the current date from the actual date on which the payment should have been made. Let's add another column in which we write a simple formula: add the number of days of deferment to the shipment date. And extend the formula to the end of the table.

According to the receivables, it turned out that IP “Karpov”, for example, should have paid the debt on February 4, and today is March 3. But the individual entrepreneur “Strigunova” still has 6 days to pay, because... its deadline is March 9.

Now let’s count the number of overdue days, remembering to change the format of the cells of the new column to numeric.

Those. from the current date we subtracted the payment date and obtained the number of overdue days. Note that cell B1 is absolute (enclosed in $ signs), so it remains the same as you drag through the formula. By the way, we got two negative values. This means that IP “Strigunova” and IP “Malyshev” still have 6 and 2 days, respectively, to make payments.

Calculation of penalties for the period of delay

Client delays should not go unpunished. Therefore, we charge a penalty of 0.1% for each day of delay. Let's multiply 0.1% by the amount of debt and the number of days overdue.

We will hide two clients without debt, highlighted in red, for now. But we won’t remove it from the list, so that when you open the same document a week later, the debt will be calculated automatically. Select both lines, right-click and select HIDE.

The broken sequence of lines reminds us that we have two more clients.

Calculation of the refinancing rate on the settlement day

The second option for calculating interest on the debt amount is depending on the refinancing rate on the day of settlement. Let's say it's 10%. We multiply the rate by the number of days overdue and the amount of debt divided by 365.

We see that the penalties with this calculation turned out to be less than with the addition of 0.1% for each day of delay. Therefore, we conclude which method of calculating interest is more profitable to indicate in the contract.

How to identify unscrupulous clients

The main thing remains: to identify the desired clients. First, let's add up the debt and penalties accrued at 0.1%.

Let's assume that legal costs are 5,000 rubles per client. Let's calculate below the amount that we can receive after filing a lawsuit against those who have a debt of more than 5000. To do this, we will need the SUMIF function.

First argument: the range in which the criterion will be searched. Second: the actual criterion, (>5000). Third: summation range (it coincides with the first). And don’t forget to subtract the hidden Strigunova and Malyshev (H12 and H13). We get 73984 rubles.

To quickly determine who should be sued, you can use the IF function. Let's write it in a new column.

You can read the formula like this: if the total amount of debt exceeds 5000 rubles (H4>5000), then we take it “to court”. Otherwise, we output a space. Thus, we have identified clients whose amount of debt exceeds legal costs.

Ulyukaev, Navka and Patrushev

Income tax refund for treatment: registration procedure and calculation of the deduction amount

Import substitution - what is it?

OSAGO minimum insurance period

Abstract: Competition, its place and role in a modern market economy Studying new material